Where to Park Emergency Fund in India — this is one of the most common and important questions for anyone who earns, saves, or invests.

Emergencies never announce themselves — medical bills, job loss, or sudden home repairs can hit anytime. The difference between calm and chaos often depends on one thing: where you parked your emergency fund.

Let’s walk through how to create and store that safety net so it’s safe, instantly available, and inflation-proof.

Want a quick, practical guide?

Read our full step-by-step guide on emergency funds — clear, India-specific, and ready to use.

Read: What Is an Emergency FundWhat Makes a True Emergency Fund

Before choosing where to park an emergency fund in India, understand its core purpose. A real emergency fund should tick these boxes:

- Instant Liquidity – Access within 24 hours.

- Capital Safety – No risk of loss due to market swings.

- Low Penalty Exit – Withdraw anytime without major costs.

- Inflation Resistance – Earn at least enough to offset inflation.

If any of these four fail, your emergency fund isn’t doing its job.

How Much Emergency Fund Should You Keep

The ideal size depends on your lifestyle and income stability:

- Salaried employees: 3–6 months of expenses.

- Self-employed or freelancers: 6–12 months.

- Families with dependents: add a buffer for medical or education emergencies.

You can use a free calculator on the RBI Money Smart website to estimate monthly obligations and plan accordingly.

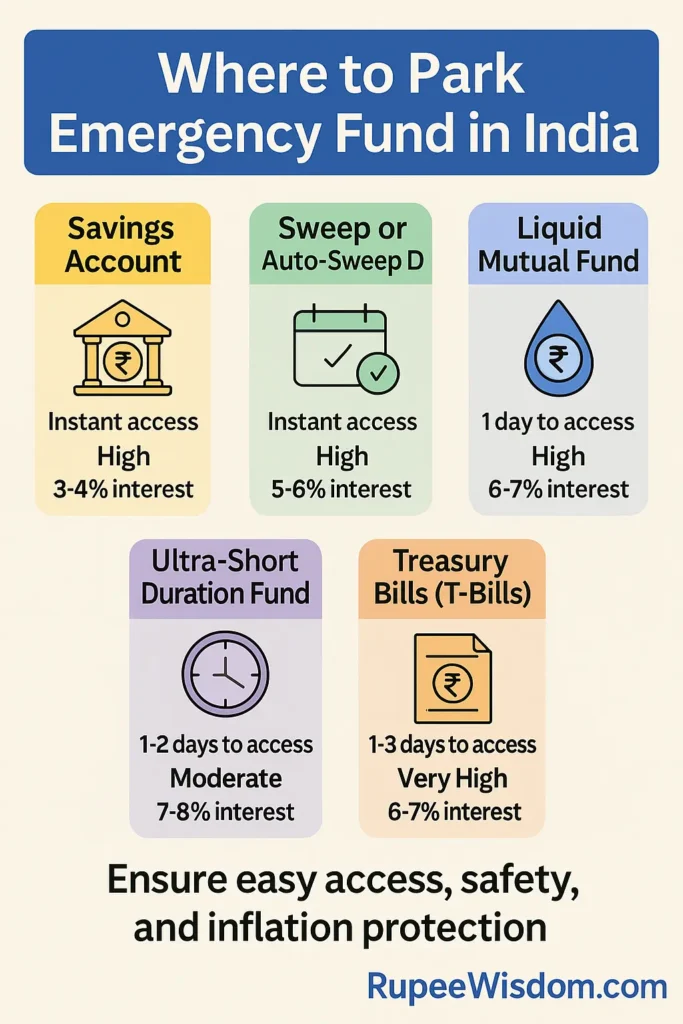

See this salary budget example for India to calculate monthly expenses.Quick Comparison: Best Places to Park Emergency Fund in India

| Option | Liquidity | Safety | Returns (Approx) | Ideal Use |

|---|---|---|---|---|

| Savings Account | Instant | Very High | 3–4% | Immediate access |

| Sweep / Auto-Sweep FD | Instant | High | 5–6% | Moderate yield + liquidity |

| Liquid Mutual Fund | 1 Day | High | 6–7% | Core emergency corpus |

| Ultra-Short Duration Fund | 1–2 Days | Moderate | 7–8% | Higher yield buffer |

| Treasury Bills (T-Bills) | 1–3 Days | Very High | 6–7% | For conservative investors |

| Digital Gold | Variable | Moderate | Fluctuates | Hedge layer (5% or less) |

Where to Park Emergency Fund in India

Savings Bank Account

This is your first layer of safety. Keep about one month of expenses here for instant withdrawals via ATM, UPI, or net banking.

Choose banks with good digital infrastructure and robust safety nets such as Deposit Insurance and Credit Guarantee Corporation (DICGC), which covers up to ₹5 lakh per depositor.

Avoid: parking your entire corpus here — low returns and inflation erode value fast.

Sweep-in or Auto-Sweep Fixed Deposit

Perfect for those who want both liquidity and returns.

Your money sits in a savings account until it crosses a limit; then it automatically “sweeps” into an FD. When you withdraw, it sweeps back instantly.

Check your bank’s partial-break policy — some split FDs into chunks (₹10,000 each) to avoid penalties.

HDFC Bank’s Sweep-in FD details and SBI’s Multi Option Deposit pages explain this feature well.

Liquid Mutual Funds

These are the best place to keep emergency fund in India for most people. They invest in short-term government and corporate debt, offering 6–7% annual returns with minimal risk.

Withdrawals settle in 24 hours, and select AMCs even provide instant redemption.

Stick with reputed fund houses regulated by SEBI and cross-check schemes on AMFI.

Pro Tip: Avoid long-duration or credit-risk funds. You want stability, not excitement.

Ultra-Short Duration Debt Funds

Slightly longer tenure than liquid funds but still low risk.

These can offer marginally higher yields (7–8%) but with mild volatility.

Use them for around 10–15% of your corpus.

Check the fund’s “Modified Duration” — anything above 6 months is not ideal for an emergency corpus.

Treasury Bills (T-Bills) & Government Securities

If you’re extremely conservative, consider T-Bills or G-Secs issued by the Government of India.

They’re virtually risk-free and available via the RBI Retail Direct portal.

Liquidity takes 1–2 business days, so use them for the long-term safety portion of your fund.

Digital Gold (Tiny Portion)

Digital gold can act as a hedge against systemic risk, but never rely on it for quick access.

If you really want exposure, limit it to 5% or less of your total fund.

Use trusted platforms backed by banks or government-recognized vaults.

How to Decide Where to Park Emergency Fund in India

Before finalizing, ask yourself:

- Do I need same-day access to the entire fund?

- Am I okay with a one-day redemption delay for better returns?

- Do I prefer guaranteed returns (FD) or market-linked (funds)?

- Am I comfortable managing online investments?

If you need instant access: use a savings account or sweep FD.

If you can wait 24 hours: use a liquid fund.

If you want higher yield: keep a small slice in ultra-short funds or T-Bills.

Balancing these ensures liquidity, safety, and returns — the holy trinity of emergency fund design.

Savings Account vs Liquid Fund

| Factor | Savings Account | Liquid Fund |

|---|---|---|

| Liquidity | Instant | 1 Business Day |

| Returns | 3–4% | 6–7% |

| Risk | None | Low |

| Taxation | Income tax slab | Capital gains |

| Ideal Use | Immediate expenses | Main corpus |

For most people, a 40:60 split between savings and liquid funds works best.

Smart Allocation Strategy

| Segment | Percentage | Instrument | Purpose |

|---|---|---|---|

| Quick Cash | 15% | Savings Account | Instant access |

| Main Corpus | 55% | Liquid Fund / Sweep FD | Safety + returns |

| Yield Buffer | 20% | Ultra-Short Fund / T-Bills | Moderate growth |

| Hedge | 10% | Digital Gold | Extreme backup |

Refill the fund after every withdrawal. Think of it as a permanent line of defense, not a one-time setup.

Real-Life Example

Rakesh, a 35-year-old from Pune, keeps ₹3 lakh aside for emergencies.

He parks ₹50,000 in a savings account, ₹2 lakh in a liquid fund, and ₹50,000 in a sweep FD.

When his car broke down unexpectedly, he redeemed from the liquid fund and received money within a day.

He didn’t touch credit cards or personal loans — proof that choosing where to park your emergency fund in India smartly really matters.

When to Revisit Your Emergency Fund

Inflation, income, and expenses change every year.

Reassess where to park your emergency fund in India every 6–12 months.

If your lifestyle cost rises by 10%, expand your corpus accordingly.

Also, review your bank’s FD and fund returns; shift if better options appear.

During major life events — marriage, childbirth, home purchase — upgrade your fund proportionately.

Common Mistakes to Avoid

- Treating credit cards as backup funds.

- Putting emergency money in equity or crypto.

- Ignoring inflation and taxation.

- Mixing emergency fund with travel savings.

- Not refilling after using it once.

Your emergency fund must be sacred — untouched except in true emergencies.

India-Specific Tips

- Use large banks or AMCs with solid ratings.

- Keep both online and offline access (UPI + ATM).

- Verify your FD coverage under DICGC.

- Don’t chase 0.5% higher return if it delays access.

- Document where your emergency corpus is stored; family should know too.

Pro Tips for Success

- Automate transfers each month.

- Keep the fund in a separate, clearly labeled account.

- Use a small SIP in a liquid fund for steady growth.

- Rebalance twice a year.

- Name the account something emotional — “Family Safety Fund” works wonders psychologically.

FAQs

1. What is the safest place to keep an emergency fund in India?

A mix of savings account and liquid mutual fund offers the perfect balance of safety, liquidity, and moderate return.

2. Can I keep my emergency fund in mutual funds?

Yes — stick to SEBI-regulated liquid or ultra-short duration funds listed on AMFI.

3. Is a fixed deposit a good emergency fund option?

Yes, but use sweep-in or breakable FDs for flexibility. Regular FDs lock your cash.

4. Should I hold gold or cryptocurrency as an emergency fund?

No. They’re volatile and difficult to liquidate instantly. Keep them separate.

5. How much emergency fund should I maintain in 2025?

At least 6 months of expenses including rent, EMIs, and healthcare. Adjust annually for inflation.

6. Can I keep my emergency fund in fintech apps?

Only if the app partners with a regulated bank or AMC under RBI or SEBI supervision. Always verify licenses on RBI’s official list.

Want to learn how to build your fund?

Read our step-by-step guide: How to Save for Emergency Fund in India — practical monthly plans, automation hacks, and milestone checkpoints to get your safety net ready fast.

Conclusion

When deciding where to park emergency fund in India, remember — no single option fits everyone.

Blend instant access with safety and modest returns.

Your savings account ensures quick cash, liquid funds grow it safely, and sweep FDs or T-Bills provide extra security.

Together, they form your financial shield against uncertainty.

Start small but start today. Build, park, and protect your fund — because when life throws surprises, your emergency fund is not just money.

It’s peace of mind.

Disclaimer: The information in this article is for educational purposes only and should not be considered financial advice. Please consult a qualified financial advisor before making any major money decisions.