If you’re googling what is alpha in mutual fund, you’re already ahead of most investors. Alpha is the single metric that tells you if your mutual fund manager actually beat the market after adjusting for risk—not just got lucky in a rising tide. In plain English: did the captain row better, or did the river just flow faster?

This master guide cuts the fluff and gets you ready to evaluate, pick, and monitor funds using alpha—without needing a finance degree or complicated math.

If you have ever wondered what is alpha in mutual fund, this guide will break it down with simple examples and practical use cases.

What Is Alpha In Mutual Fund (and why it matters)

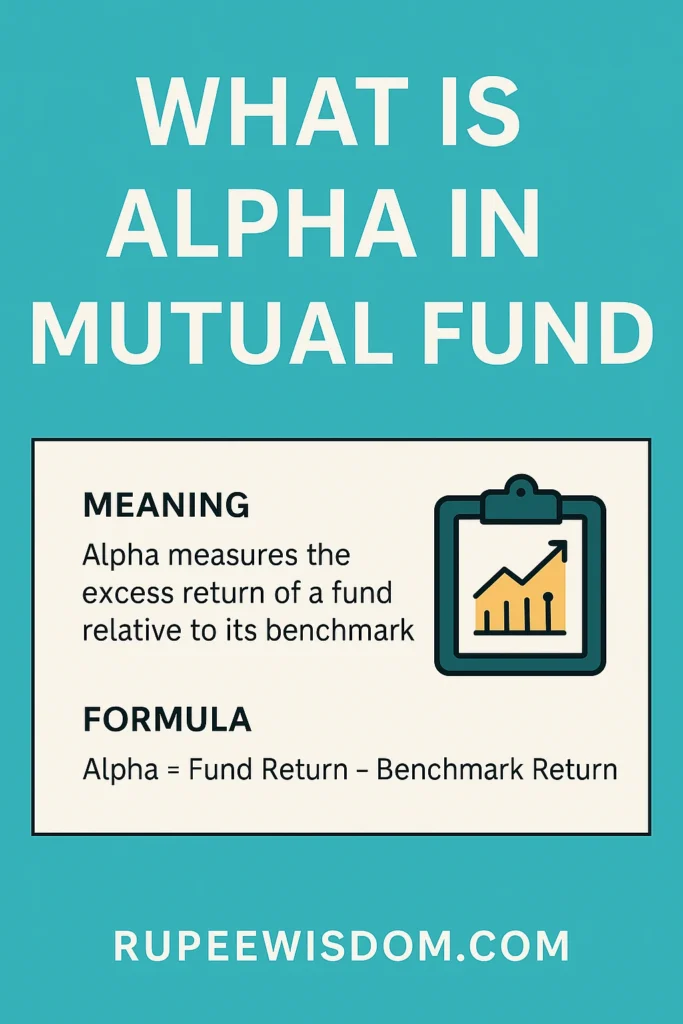

Alpha measures the excess return a fund generated over its benchmark after accounting for market risk.

- Positive alpha → Outperformance (manager added value).

- Zero alpha → You basically got the benchmark (why pay high fees?).

- Negative alpha → Underperformance (you paid extra to get less).

Bottom line: If you pay for active management, demand sustained positive alpha. If not, low-cost index funds exist for a reason.

A Quick History Of Alpha (Why it was created)

Alpha didn’t pop out of nowhere—it comes from financial research in the 1960s. Michael Jensen, an economist, introduced “Jensen’s Alpha” in 1968 to measure how mutual fund managers performed against the market after accounting for risk.

Until then, investors mostly looked at raw returns, which is misleading. A risky portfolio might look great in a bull market, but it’s not real skill if the same risk brings huge losses later.

Jensen’s Alpha solved this by adjusting returns for risk, giving investors a fair way to judge skill vs luck. Today, it’s still the global standard for measuring fund performance.

The Alpha Formula (Made Ultra-Simple)

The full version (from CAPM) looks like this:

Alpha = Fund Return – [Risk-Free Rate + Beta × (Market Return – Risk-Free Rate)]

Simplified:

Alpha = Fund’s return – Benchmark’s return (after adjusting for risk)

Example

- Fund return: 15%

- Benchmark return: 12%

- After adjusting for risk, expected return: 12.6%

- Alpha = 15% – 12.6% = +2.4%

That +2.4% is the “extra marks” your fund manager scored beyond what the market itself would have given.

Understanding what is alpha in mutual fund through this formula helps investors see whether returns are due to skill or just market movement

Good Alpha vs Bad Alpha

- +1% to +3% alpha sustained over 3–5+ years is solid.

- More than +3% consistently is rare; investigate how it’s earned.

- Negative alpha over long windows is a red flag.

One year of alpha is noise. Rolling 3–5 year periods are the real test.

Alpha vs Beta vs Sharpe vs R-Squared

- Alpha: Extra return beyond benchmark after adjusting for risk.

- Beta: Fund’s sensitivity to market moves.

- Sharpe: Return per unit of volatility.

- R-Squared: How well the benchmark actually explains the fund’s movement.

Think of it like cricket:

- Alpha = Runs above team average.

- Beta = Aggressiveness of batting.

- Sharpe = Runs per chance of dismissal.

- R-Squared = Did the batsman adapt to pitch conditions?

Where Alpha Shines (and where it misleads)

Alpha works when:

- Benchmark is correct.

- Tested over 3–5 years (not one year).

- Fees are reasonable.

Alpha misleads when:

- Wrong benchmark is used.

- Period cherry-picks a bull run.

- R² is too low (benchmark not relevant).

Practical Indian Mutual Fund Alpha Ranges

To fully grasp what is alpha in mutual fund, it’s important to see how alpha varies across large-cap, flexi-cap, mid-cap, and small-cap categories in India.

- Large-cap funds: Alpha is usually small, often 0% to +2%. Hard for managers to beat Nifty 50/100 consistently.

- Flexi/Multi-cap funds: Better chance to generate alpha, often +1% to +3% in rolling periods.

- Mid-cap funds: Can produce higher alpha (+2% to +5%), but risk and volatility are higher.

- Small-cap funds: Alpha can look impressive (+4% to +6%), but cycles are brutal; losses in downturns can wipe gains.

- Sectoral funds: Alpha often looks large but is tied to one sector’s performance, not manager skill.

This is why context matters: a +2% alpha in large-cap is more impressive than +5% alpha in small-cap.

For investors, SEBI’s mutual fund regulations govern how performance reporting is standardized in India

Using Alpha To Pick Funds (Step-by-step)

- Choose category based on your goal.

- Find relevant benchmark (Nifty 50, Nifty 500, etc.).

- Check rolling 3-yr alpha over 5–7 years.

- Confirm beta (0.8–1.2 range is healthy).

- Look for high R² (above 70–80).

- Cross-check standard deviation and Sharpe ratio.

- Make sure expense ratio doesn’t wipe out alpha.

What Is Alpha In Mutual Fund Selection? (Worked comparison)

| Signal | Fund A | Fund B |

|---|---|---|

| Rolling 3-yr alpha (5-yr window) | 74% positive | 38% positive |

| Median alpha | +1.4% | +0.3% |

| Beta | 0.95–1.08 | 1.18–1.35 |

| R² | 0.88 | 0.63 |

| Standard deviation | 16% | 21% |

| Max drawdown | −21% | −29% |

Fund A shows truer, consistent alpha. Fund B is more risky and inconsistent.

How Much Alpha Matters In Numbers

10 lakh invested for 10 years:

- Index fund at 11% CAGR → 28.4 lakh

- Active fund at 12% CAGR (+1% alpha) → 31.1 lakh

Extra alpha of 1% = 2.7 lakh more wealth, with no extra work.

Myths vs Facts About Alpha

Myth: High alpha always means great manager.

Fact: Sometimes it’s just higher beta or lucky sector bets.

Myth: Alpha in one year proves skill.

Fact: Skill shows up only in rolling 3–5 year periods.

Myth: Any alpha is worth higher fees.

Fact: If fees eat it up, you gain nothing.

Myth: Alpha is all you need.

Fact: Always pair with beta, SD, Sharpe.

Mini Glossary

- Alpha: Extra return above benchmark, after risk.

- Beta: Sensitivity to market movement.

- Sharpe Ratio: Return per unit of risk.

- Standard Deviation: How volatile returns are.

- R-Squared: Fit between fund and benchmark.

- Drawdown: Peak-to-trough fall during a market drop.

FAQs

Is higher alpha always better?

Yes, if consistent.

Can alpha be compared across categories?

No, only within the same category.

What’s a good alpha in India?

+1% to +3% over 3–5 years.

Do index funds have alpha?

No, they aim for zero alpha.

Should I exit after one bad year?

No. Look at rolling periods.

Conclusion

The real answer to what is alpha in mutual fund lies in seeing whether your manager consistently adds value beyond the benchmark.

Alpha is not just jargon. It’s your tool to judge if your mutual fund manager really added value or simply rode the market wave.

- Positive alpha means genuine outperformance.

- Zero alpha means you’d be better off with an index fund.

- Negative alpha means wasted fees and underperformance.

But alpha is not everything. Always check it alongside beta, standard deviation, Sharpe, and fees. Look for consistent performance over 3–5 years, not just one-year stars.

For Indian investors:

- Large-cap: Passive often wins.

- Flexi/Multi-cap: Hunt for steady alpha.

- Mid/Small-cap: Expect alpha but prepare for bigger swings.

Final word: Alpha is proof, not hype. If your fund shows it consistently, stay invested. If not, go passive and let compounding work for you.

Now you’ll never need to ask “what is alpha in mutual fund” again—you can use it smarter than most investors out there.