Struggling to stretch a ₹30,000 take-home across rent, EMIs, groceries, and still save? You’re not alone. “30 hazaar mein budget kaise banaye” is a real Indian problem. This guide gives you a grounded, numbers-first plan that works in Tier-1 and Tier-2/3 cities, with and without EMIs—plus downloadable structures you can replicate every month.

What you’ll get here (no fluff):

- A core budget formula tuned for India (with exact rupee splits).

- Two ready models: with EMI and without EMI.

- City-tier adjustments (rent & commute swing a lot).

- A mini debt-clear plan for multiple EMIs.

- A simple one-page template you can implement tonight.

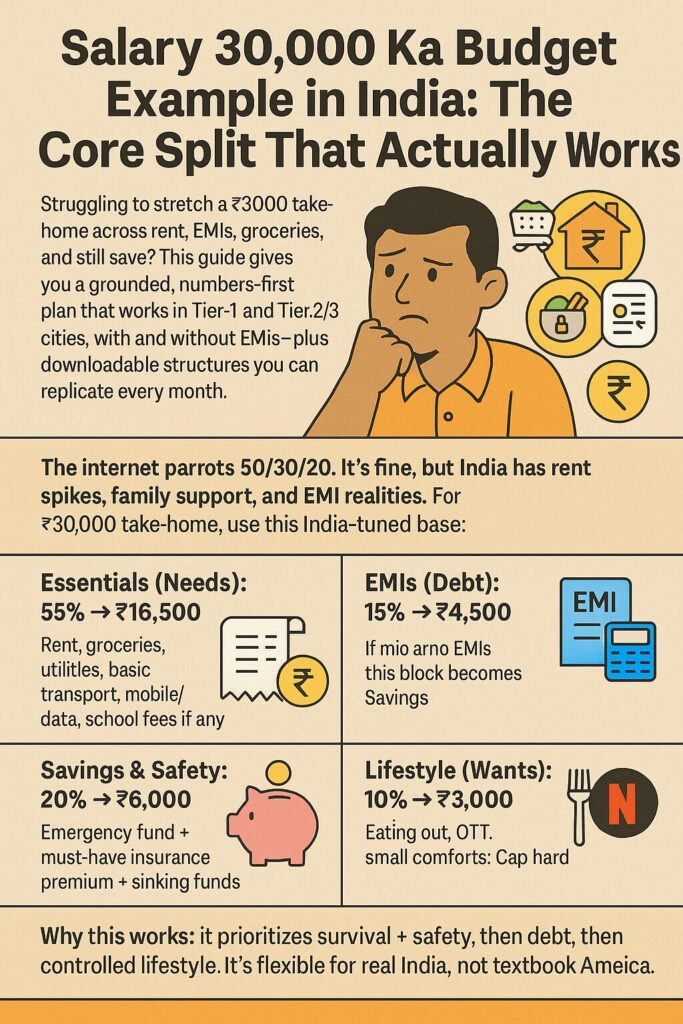

Salary 30,000 Ka Budget Example in India: The Core Split That Actually Works

The internet parrots 50/30/20. It’s fine, but India has rent spikes, family support, and EMI realities. For ₹30,000 take-home, use this India-tuned base:

- Essentials (Needs): 55% → ₹16,500

Rent, groceries, utilities, basic transport, mobile/data, school fees if any. - EMIs (Debt): 15% → ₹4,500

If you have no EMIs, this block becomes Savings. - Savings & Safety: 20% → ₹6,000

Emergency fund + must-have insurance premium + sinking funds. - Lifestyle (Wants): 10% → ₹3,000

Eating out, OTT, small comforts. Cap hard.

Why this works: it prioritizes survival + safety, then debt, then controlled lifestyle. It’s flexible for real India, not textbook America.

Read more: How to budget your salary

Salary 30,000 Ka Budget Example in India: Exact Line-Item Budget (No EMI Case)

Profile: Single/Tier-2 city, no EMI, sharing accommodation or living with family.

| Category | Amount (₹) | Why this cap works |

|---|---|---|

| Rent/Household share | 6,000 | Roommate/PG/family contribution. Avoid >₹7,000. |

| Groceries + Home supplies | 4,000 | Plan weekly menus; fixed ₹1,000/week. |

| Utilities (power, LPG, water) | 1,200 | Track units; avoid vampire loads; prepaid if possible. |

| Mobile + Data + OTT | 600 | Keep OTT annual + split with friends. |

| Local transport | 1,500 | Monthly pass/metro card. |

| Essentials subtotal | 13,300 | Leaves headroom for spikes. |

| Health insurance premium | 800–1,000 | Even a basic cover > zero cover. |

| Emergency fund (EF) | 3,000 | Auto-transfer to EF bucket (explained later). |

| Sinking funds (fees, travel, gifts) | 2,000 | Prevents “oops” months. |

| Savings & Safety subtotal | 6,000 | Non-negotiable. |

| Lifestyle | 3,000 | Cash envelope. When it’s over, it’s over. |

| Buffer (spillover/misc) | 1,700 | Absorbs electricity spike/medicine. |

| Total | ₹30,000 | Balanced, resilient. |

Implementation tip: Open three buckets (separate accounts or sub-accounts): Bills, Savings, Spends. On salary day, auto-sweep set amounts to each. No willpower required.

Salary 30,000 Ka Budget Example in India: Exact Line-Item Budget (With EMI)

Profile: Tier-1/Tier-2, one active EMI (phone/personal/education).

| Category | Amount (₹) | Tactics |

|---|---|---|

| Rent/Household | 7,000 | Shared 2/3-BHK or family contribution. |

| Groceries | 4,000 | Switch to weekly cash envelope. |

| Utilities | 1,200 | Prepaid + usage audit. |

| Mobile/Data/OTT | 500 | Family postpaid add-on or annual OTT split. |

| Transport | 1,300 | Mixed: metro pass + occasional cab. |

| Essentials subtotal | 14,000 | |

| EMI(s) | 4,500 | Keep total EMI ≤15% while income is low. |

| Health insurance | 800–1,000 | Protects EF from hospital shocks. |

| Emergency fund | 2,500 | Lower for now, but non-zero. |

| Sinking funds | 1,500 | Fees, repairs, festivals. |

| Savings & Safety subtotal | ~₹5,800 | |

| Lifestyle | 2,700 | Cash-only. Zero rollovers. |

| Total | ₹30,000 |

Can’t keep EMI at 15%? Then cut rent (roommate), or move to a debt-first phase (see below) for 90–120 days.

Salary 30,000 Ka Budget Example in India: City-Tier Tweaks (Rent & Commute)

- Tier-1 (Metro): Push rent to ₹8–9k by sharing; shave transport with metro. Cut lifestyle to ₹2k.

- Tier-2: Keep rent ₹5–7k, but watch commute (autos stack up).

- Living with parents: Skip rent, redirect ₹5–7k to EF + insurance. You’ll build safety fast.

Negotiation hacks:

- Pick non-prime localities near a metro line, not near office hubs.

- Annual payment for data/OTT (cheap in bulk).

- Meal-prep Sundays: one big cook saves ₹1,000–₹1,500/month.

Salary 30,000 Ka Budget Example in India: Emergency Fund (Start Tiny, Win Big)

Target: Start with ₹15,000 (half-month), then ₹45,000 (1.5 months), ultimately ₹90,000 (3 months).

Parking: 50% high-liquidity savings + 50% liquid/ultra-short mutual fund (avoid equity for EF).

Automation: Set ₹2,500–₹3,000 auto-transfer on salary+1 day.

Rule: If you dip into EF, replenish first before any new gadget/holiday.

Salary 30,000 Ka Budget Example in India: Insurance Minimums You Shouldn’t Skip

- Health insurance: Even a ₹3–5 lakh base plan beats zero. Premium can fit in ₹800–1,000/month range (age-dependent).

- Term life (only if dependents): Start with a small cover; premiums are low at younger ages.

- Why here? One medical bill can nuke your EF and push you back into debt. Insurance is EF’s bodyguard.

Salary 30,000 Ka Budget Example in India: Two Debt-Clear Frameworks (Pick One)

When you have multiple EMIs or lingering card dues, choose a lane and don’t switch mid-ride.

1) Avalanche (Mathematicians’ favorite)

- Pay minimums on all loans.

- Throw every extra rupee at the highest interest loan (usually credit card > personal loan > consumer loan).

- Mathematically cheapest; needs discipline.

2) Snowball (Motivation hack)

- Pay minimums on all loans.

- Attack the smallest balance first, close it, feel the win, roll that EMI into the next.

- Slightly costlier, often easier to stick with.

90-Day “Debt Sprint” plan (on ₹30k):

- Slash lifestyle to ₹1,000–1,500 for 3 months.

- Push extra ₹1,500–2,000/month to your chosen method.

- Sell unused stuff (phones, gadgets) → one-time ₹3–8k prepayment.

- Call lenders, negotiate lower APR or a hardship plan—you’ll be surprised.

Salary 30,000 Ka Budget Example in India: 50/30/20 vs India-Tuned Model

When 50/30/20 works: No EMI, lower rent (parents/PG), stable job.

When India-tuned 55/15/20/10 wins: High rent city or any EMI present.

Upgrade rule: Each time your take-home jumps by ₹5,000, review caps (especially EF & insurance). Lifestyle creeps silently—guard against it.

Salary 30,000 Ka Budget Example in India: The One-Page Monthly Template

On Salary Day (T+0):

- Land ₹30,000 in Salary account.

- Auto-transfer same day:

- Bills/Essentials: ₹14,000–₹16,500 → dedicated “Bills” account.

- Savings & Safety: ₹6,000 → “Safety” account (EF + insurance).

- EMIs: ₹0–₹4,500 → loan bank mandates.

- Spends: Balance to “Spends” account (UPI card or prepaid card).

- Cash Envelopes (optional): Groceries ₹1,000/week + Lifestyle ₹3,000/month.

Mid-Month (T+15):

- 15-minute audit: If Groceries overshoot, shave next week. If UPI shows “Zomato attacks,” pause eating out for 7 days.

Month End (T+27–T+29):

- Whatever remains in Spends → move 50% to EF, 50% to Sinking Funds.

Salary 30,000 Ka Budget Example in India: Real-Life Scenarios (Pick Yours)

A) Paying PG + One EMI (Phone)

- Keep rent ≤₹7k (shared room).

- Lifestyle down to ₹1.5–2k for 90 days → snowball the phone loan.

- After closure, redirect the EMI to EF for two full months before any upgrade.

B) Living With Parents, No EMI

- Push EF to ₹45,000 within 6–7 months (₹6k/month).

- Start a small recurring deposit (RD) of ₹1,000 for festival/annual expenses.

- Invest only after EF ≥ 1.5 months and health insurance is active.

C) Married, One Income, Child Schooling

- Essentials jump; squeeze lifestyle to ₹1–1.5k.

- Build three sinking funds: Fees, Medical, Festival.

- Target EF to ₹90,000 (3 months) even if it takes a year. Stability > speed.

Salary 30,000 Ka Budget Example in India: 12 “Tiny Wins” That Save ₹2,500–₹4,000/Month

- Annual mobile/data + shared OTT.

- Commute pass (metro/bus) vs ad-hoc rides.

- Meal-prep + bulk staples (dal, rice, oil).

- Shift one paid habit to free (gym → park workouts for 90 days).

- Seasonal veggies + local brands for staples.

- Stop “convenience fees”: pay utilities via fee-free routes.

- Avoid BNPL for small purchases (fees stack).

- Use cash for lifestyle; end of envelope = end of spends.

- Keep one UPI for bills, one for spends (mental separation).

- Maintain a medicine kit at home—saves sudden pharmacy runs.

- Buy reusable (steel bottles, lunch boxes) to cut tiny repeats.

- Run a 7-day “No Spend” challenge once a month.

Salary 30,000 Ka Budget Example in India: When to Increase Savings or Lifestyle

- Increase Savings when:

- You get a raise/bonus.

- A loan closes (roll EMI into EF for two months before any upgrade).

- Family responsibilities increase (new dependent).

- Increase Lifestyle only when:

- EF ≥ 1.5 months of expenses and insurance in force.

- You’ve completed a 90-day debt sprint.

- You can add ₹500–₹1,000 to lifestyle without cutting EF.

Salary 30,000 Ka Budget Example in India: FAQ (Super Quick)

Q: 50/30/20 or India-tuned 55/15/20/10?

A: Start with 55/15/20/10 if you pay rent or have EMIs. Move to 50/30/20 only when EF is on track and no EMI pressure.

Q: How big should my EF be at ₹30k salary?

A: Start with ₹15k, push to ₹45k, then ₹90k (3 months). Pace > perfection.

Q: Invest while building EF?

A: If no EF, first ₹10–15k must be EF. After that, you can split (e.g., ₹2,000 EF + ₹1,000 RD/SIP).

Q: Multiple EMIs—what first?

A: Close the smallest or highest-interest first (pick one method and stick for 90 days).

Q: Can I keep EF in a savings account only?

A: Start there for liquidity, but move half to liquid/ultra-short funds once EF > ₹15k to beat idle cash drag.

Salary 30,000 Ka Budget Example in India: Your 7-Day Kickstart Plan

Day 1: Open/identify Bills, Safety, Spends accounts.

Day 2: Set auto-transfers (₹ value from your model above).

Day 3: List EMIs, interest, balances; choose Avalanche or Snowball.

Day 4: Build a ₹1,000 starter EF (sell one unused item if needed).

Day 5: Annualize data + OTT, split with family/friends.

Day 6: Buy basic health insurance if you don’t have it.

Day 7: Weekly grocery plan + cash envelopes kick in.

Repeat for four weeks. Then review and rebalance.

Final Word

A ₹30,000 salary is tight, but not impossible. The winning combo is automation + hard caps + tiny wins. Follow the model for 90 days, and you’ll feel the pressure drop: EMIs stabilize, EF grows, lifestyle stops leaking. When income rises, don’t inflate; upgrade EF and insurance first, then give lifestyle a small raise.