LIC is India’s most trusted insurer, and one of its flagship policies is Jeevan Umang. It’s a unique mix of life insurance + savings + guaranteed yearly income.

But before buying, the real question is:

👉 How much premium will I pay?

👉 When will my yearly income start?

👉 What’s my maturity value and real return (IRR)?

The fastest way to answer these is by using a Jeevan Umang Calculator.

Quick heads-up: The old Plan 945 is withdrawn. The current active version is Plan 745 (UIN: 512N312V03). Always check that your calculator is updated for Plan 745.

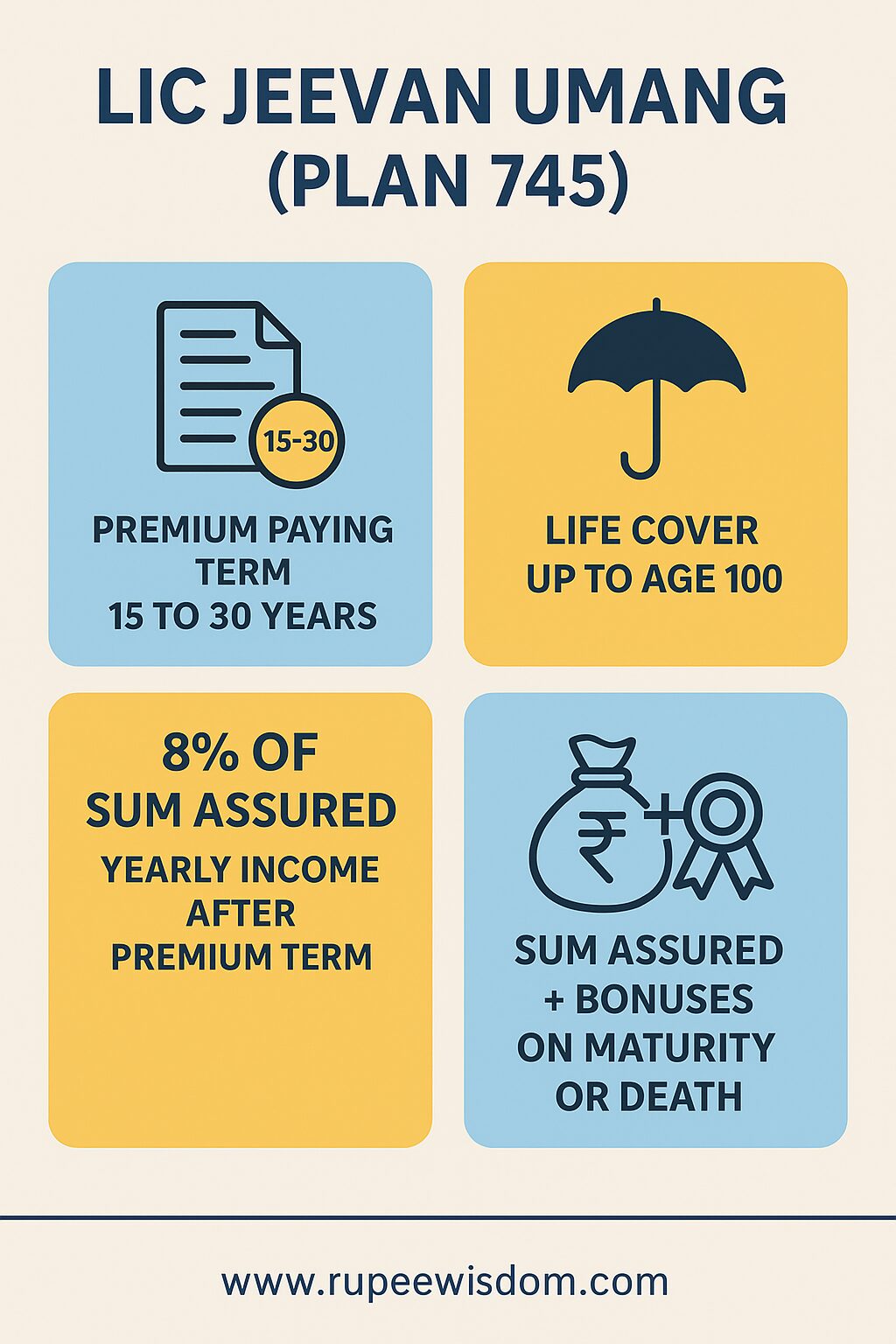

What is LIC Jeevan Umang (Plan 745)?

In the simplest words:

- Pay premiums for 15, 20, 25, or 30 years (you choose).

- After the premium-paying term ends, LIC pays you 8% of Basic Sum Assured every year (called Survival Benefit).

- This continues till you turn 100 or till death.

- On maturity at 100 (or death earlier), LIC pays Sum Assured + bonuses in lump sum.

So you get:

✔ Lifetime yearly income

✔ Life cover till 100

✔ Final maturity/death payout

For full, authoritative detail straight from LIC, refer to their official Jeevan Umang Sales Brochure (Plan 745).

Why Use a Jeevan Umang Calculator?

The calculator helps you:

- Know your exact premium (monthly/quarterly/yearly).

- See 8% yearly income clearly.

- Get IRR (Internal Rate of Return) to compare with FD, term + mutual fund, etc.

- See bonus scenarios (conservative/average/optimistic).

- View year-by-year cashflows—so there are no surprises.

Jeevan Umang IRR vs Alternatives (Quick Visual)

The IRR (Internal Rate of Return) is the best apples-to-apples way to compare Jeevan Umang with other options. Below is an illustrative range comparison. Your actual IRR will depend on your age, premium mode, bonus outcomes, and holding period.

| Option | Typical IRR Range (Illustrative) | Risk / Notes |

|---|---|---|

| Jeevan Umang (Plan 745) | ~4% – 6% | Participating bonuses vary; strong income certainty post-PPT |

| Bank FD (5–10 yrs) | ~6% – 7% | Taxable interest; high safety |

| PPF (15 yrs) | ~7% – 8% | Sovereign-backed; EEE tax treatment |

| Debt Mutual Fund | ~6% – 8% | Market-linked; indexation rules apply as per current tax law |

| Equity Mutual Fund (long term) | ~10% – 12%+ | Volatile; potential for higher returns with risk |

Note: Ranges above are educational and rounded. Tax treatment, tenure, and risk can change your real, post-tax return. Always compare your personalized IRR from the Jeevan Umang calculator before deciding.

Example: Jeevan Umang Calculator in Action

Case Example

- Age: 30 years

- Basic Sum Assured (BSA): ₹10,00,000

- Premium Paying Term (PPT): 20 years

- Mode: Yearly

Calculator Output:

- Premium: Around ₹47,000 per year (varies slightly with GST).

- Survival Benefit: ₹80,000 per year (8% of 10 lakh) from year 21 till age 100.

- Bonuses: Added at maturity (not guaranteed).

- Maturity/Death: ₹10 lakh + accumulated bonuses.

Year-by-Year Illustration (Sample)

Here’s how a Jeevan Umang calculator table might look for the above case (simplified, bonuses not included):

| Policy Year | Age | Premium Paid | Survival Benefit (8% of SA) | Cumulative Survival Benefits |

|---|---|---|---|---|

| 1–20 | 30–49 | ₹47,000/yr | Nil | Nil |

| 21 | 50 | Nil | ₹80,000 | ₹80,000 |

| 22 | 51 | Nil | ₹80,000 | ₹1,60,000 |

| 23 | 52 | Nil | ₹80,000 | ₹2,40,000 |

| … | … | … | … | … |

| 70 | 99 | Nil | ₹80,000 | ₹16,00,000+ |

| 71 (Maturity) | 100 | Nil | ₹80,000 | ₹16,80,000 + Maturity (₹10L + Bonus) |

👉 By age 100, you’d have already received ₹16.8 lakh in yearly income + final lump sum. That’s the power of long-term income.

Jeevan Umang (745) vs Jeevan Utsav vs Term+MF

| Feature | Jeevan Umang (745) | Jeevan Utsav | Term Plan + Mutual Fund |

|---|---|---|---|

| Type | Whole life + savings | Limited premium, guaranteed income | Pure protection + market investment |

| Yearly Income | 8% of SA (post PPT) | Guaranteed % payouts for limited years | Depends on MF returns |

| Life Cover | Till 100 | Till 100 | Till chosen term |

| Liquidity | Limited | Moderate | High (MFs can be redeemed) |

| IRR | 4–6% (depends on bonuses) | 5–7% (structured payouts) | 8–12% (if equities do well) |

| Risk | Very low | Low-medium | Market risk |

👉 If you want guaranteed income for life, Umang wins. If you want higher returns, Term + MF combo may suit better.

Pros of Jeevan Umang

✔ Guaranteed yearly income (8% of SA)

✔ Life cover till age 100

✔ Lump sum maturity/death payout

✔ Eligible for LIC bonuses

✔ Loan facility

✔ Tax benefits (80C, 10(10D))

Cons of Jeevan Umang

✘ Premiums are higher than pure term plans

✘ Bonuses are not guaranteed

✘ Returns (IRR) are moderate (usually ~4–6%)

✘ Liquidity is low (surrendering early isn’t wise)

Who Should Consider Jeevan Umang?

✅ Parents wanting steady income for future needs

✅ Retirees or near-retirees who prefer predictable income

✅ Risk-averse investors who don’t want equity exposure

✅ People looking for cover till 100 years

❌ Not ideal for aggressive investors chasing high returns

❌ Not for those who may need liquidity in short term

How to Use a Jeevan Umang Calculator (Step-by-Step)

- Enter your age.

- Choose premium paying term (15/20/25/30).

- Enter Basic Sum Assured.

- Select payment mode (annual, half, quarterly, monthly).

- Calculator shows: premium, survival benefit, maturity.

- Check bonus scenarios.

- Look at IRR.

- Download or email the report.

- Adjust inputs until it matches your goal.

FAQs on Jeevan Umang Calculator

Q1: Is the 8% in Jeevan Umang a return?

No. It’s a payout on Sum Assured, not the investment return. IRR is lower.

Q2: Is Plan 945 still available?

No. It’s withdrawn. Only Plan 745 is active.

Q3: Are bonuses guaranteed?

No. They depend on LIC’s annual declaration.

Q4: When do survival benefits start?

Immediately after the premium paying term ends.

Q5: Can I take a loan?

Yes, after certain conditions.

Q6: Is the calculator accurate?

Premiums and payouts are accurate. Bonuses are assumptions.

Misconceptions People Have

❌ “8% is return” → Wrong. It’s payout, not IRR.

❌ “Plan 945 still works” → Wrong. Withdrawn.

❌ “Bonuses are fixed” → Wrong. Variable every year.

What Makes a Good Jeevan Umang Calculator?

- Clean inputs (age, PPT, SA, mode)

- Shows premium clearly

- Displays 8% benefit timing & amount

- Provides bonus scenarios

- Calculates IRR

- Year-by-year table

- Option to download/email report

- Transparent disclaimers

Final Thoughts

LIC Jeevan Umang is a plan for those who want predictable yearly income + lifetime cover. It’s not a “get-rich” product, but a peace-of-mind plan.

Using a Jeevan Umang calculator before investing is non-negotiable. It shows you exactly:

- Premiums you’ll pay

- Yearly income you’ll receive

- Maturity payout scenarios

- IRR so you know the real return

If you want high returns, look at term + MF combo. If you only want cover, buy a term plan. But if safety + guaranteed income for life sounds right, Jeevan Umang fits.

👉 Bottom line: Run the calculator, know your numbers, then decide.