If you’ve been searching for How to Start Investing in India, let me tell you something honestly — you’re already doing better than most people.

Most Indians WANT to invest…

But they don’t start because of fear, confusion, or bad advice.

One friend says “Crypto le lo.”

Your banker says “Guaranteed plan le lo.”

YouTube says “Smallcap will make you rich.”

Instagram promises “Retire at 30.”

Your uncle says “FD hi best.”

No wonder beginners get stuck.

Here’s the truth:

Investing is not complicated. The noise around it is.

This guide will show you exactly how to start investing in India 2025, step by step, even if:

- you earn ₹20k–₹30k

- you’re scared of losing money

- you’ve never opened a Demat account

- you don’t understand mutual funds

- you think “Investing is only for rich people”

Relax.

Everything will become clear in the next few minutes.

By the end of this guide, you’ll know:

- how to start investing in India practically

- which product to start with

- how much to invest

- how to build a beginner portfolio

- what mistakes to avoid

- how long to stay invested

- and most importantly… what NOT to touch at all

Let’s begin your journey the right way.

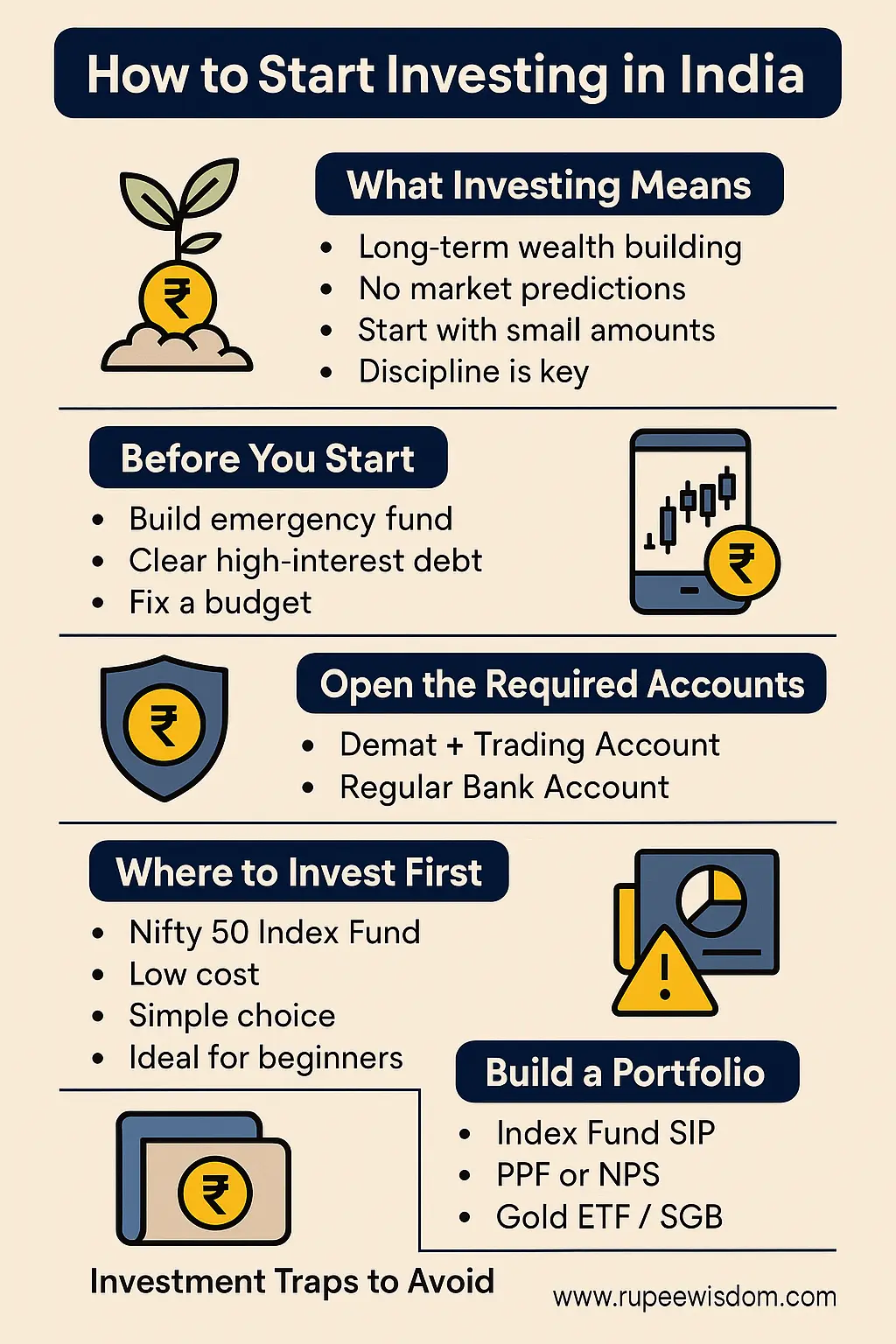

What Investing Really Means (And What It Doesn’t)

Most beginners confuse investing with trading.

That’s where fear comes from.

If you want to refresh your fundamentals before you begin, here’s a helpful overview of financial literacy basics from a trusted global resource.

Let’s simplify:

Trading = Short-term speculation

Fast profits, fast losses, fast stress.

Investing = Long-term wealth building

Slow, steady, reliable growth.

If you want to grow wealth over 5–20 years, this is where you belong.

When learning how to start investing in India, remember:

- You don’t need to predict markets

- You don’t need to time the bottom

- You don’t need expert-level finance knowledge

- You don’t need lakhs to begin

- You only need discipline + a simple plan

Investing is like planting a mango tree —

it looks slow in the beginning…

then one day, it changes your entire financial life.

Before You Start Investing: Build Your Foundation

This is the part everyone skips — and then regrets.

Beginners lose money not because investing is risky…

but because they started without a base.

If you want to truly understand how to start investing in India, build these three pillars first.

1. Build an Emergency Fund

Minimum: 3 months of expenses

Ideal: 6 months

Why?

Because if something unexpected happens:

- job loss

- medical emergency

- sudden big expenses

- home/vehicle repair

…you won’t touch your investments.

Where to park it?

- Savings account

- Liquid fund

- Sweep-in FD

Related reading: Emergency Fund Guide

This is your safety net — without it, investing becomes emotional and unstable.

2. Clear High-Interest Debt (Non-Negotiable)

If you have:

- credit card outstanding

- BNPL

- late EMI

- personal loan at 16–36%

Stop everything.

Clear this first.

Nothing — absolutely NOTHING — grows faster than credit card interest.

So before diving into how to start investing in India 2025, clean your financial ground.

3. Fix a Simple Budget

Without a budget, you’ll invest for 2 months and stop in the 3rd.

Budget protects your SIP.

To build a simple monthly plan, read this How to Budget Your Salary in India guide.

Budget = control

Control = consistency

Consistency = wealth

Even ₹500 SIP grows into lakhs when done consistently.

Most beginners mix saving and investing together, but they are different habits. If you want to strengthen your basic money habits first, here’s a simple guide on how to save money in India.

Open the Required Accounts

To actually start investing, you need:

Demat + Trading Account

To buy:

- mutual funds

- index funds

- stocks

- ETFs

- SGBs

Recommended beginner-friendly brokers:

- Groww

- Zerodha

- Upstox

10–15 minutes → account ready.

Your Regular Bank Account

Used to automate SIPs.

Automation = zero effort investing.

How Much Should You Invest?

The simplest formula:

Invest 20% of your take-home salary.

Examples:

| Salary | Monthly Investment |

|---|---|

| ₹20,000 | ₹4,000 |

| ₹30,000 | ₹6,000 |

| ₹50,000 | ₹10,000 |

| ₹1,00,000 | ₹20,000 |

But if you cannot start with 20%, begin with ₹500–₹1,000.

You’re not proving anything to anyone.

You’re building a habit.

This is exactly how to start investing in India realistically.

Where Should Beginners Invest First? (The Clean Starting Point)

Most new investors get stuck here — they open apps, see 100 funds, 20 options, and freeze.

Let me simplify:

Every Indian beginner should start with a Nifty 50 Index Fund.

Why?

- low cost

- steady, predictable long-term returns

- no expert knowledge needed

- beats most actively managed funds

- ideal for beginners

- perfect for long-term

One SIP.

One index fund.

One decision.

This alone changes your life.

If you want to understand why index funds work so well for beginners, here’s the best mutual fund strategy for early retirement that fits perfectly with a Nifty 50 SIP.

If mutual fund terms like returns, alpha or performance metrics confuse you, here’s a simple guide on what alpha means in mutual funds so you understand how funds are evaluated.

PPF — The Strongest Safe Investment for Long-Term

If you want:

- stability

- guaranteed returns

- tax benefits

- zero market risk

PPF is a must-have.

Good for people scared of the stock market.

NPS — The Retirement + Tax Saver Combo

If you’re salaried or self-employed:

- great for retirement

- disciplined long-term investing

- extra tax benefit under 80CCD(1B)

Use it alongside SIP.

Gold ETF / SGB — The Smart Way to Add Gold

Do NOT buy jewellery.

Do NOT buy physical gold as investment.

Buy:

- Gold ETF

- Sovereign Gold Bond

Keep 5–10%.

Gold protects your portfolio during market downturns.

Your First Beginner-Friendly Portfolio (Pick One)

Balanced Beginner Portfolio

- 70% Nifty 50

- 20% PPF/NPS

- 10% Gold ETF

Conservative Portfolio

- 60% PPF/NPS

- 30% Nifty 50

- 10% Gold

High-Growth Young Portfolio

- 80% Nifty 50

- 20% Gold/Debt Fund

This is exactly how to start investing in India 2025 without unnecessary complexity.

Choosing Investments Based on Your Salary

Salary Below ₹25,000

- Start with ₹500–₹1,000 SIP

- Build emergency fund

- Avoid stocks & crypto

₹25,000–₹50,000 Salary

- Index Fund SIP

- Add PPF or NPS

- Build 3–6 month emergency buffer

If your income is around ₹30,000 per month, you’ll find this salary 30,000 budget plan helpful for balancing expenses, savings, and your first SIP.

₹50,000–₹1,00,000 Salary

- Increase SIP to 25–35%

- Add Gold ETF

- Add ELSS for tax saving

₹1 Lakh+ Salary

- Build diversified portfolio

- NPS Tier 1

- Strategic long-term planning

This salary-based method gives clarity and removes guesswork.

Identify Your Risk Profile

A simple 30-second test to understand how to start investing in India based on your personality.

Low Risk (Safe Personality)

Prefer:

- PPF

- NPS

- Debt funds

- Index funds

Medium Risk

Prefer:

- Index + Debt + Gold

High Risk

Prefer:

- Index + Gold + Small-cap (very small %)

Invest according to your temperament — not greed or fear.

Investment Traps Indians Must Avoid

These are the wealth killers. Stay FAR away.

❌ ULIPs

❌ Guaranteed return policies

❌ Endowment insurance plans

❌ Penny stocks

❌ Stock tips groups

❌ Futures, options, trading

❌ Crypto (for beginners)

❌ Borrowing to invest

❌ 8 mutual funds at once

Avoiding these mistakes is half the game.

How Much Your Money Can Grow (A Realistic India Example)

Here’s a simple table to understand why starting early matters when learning how to start investing in India:

If you invest ₹5,000/month at 12% return:

| Duration | Total Invested | Expected Value |

|---|---|---|

| 10 years | ₹6,00,000 | ₹11–12 lakh |

| 15 years | ₹9,00,000 | ₹23–25 lakh |

| 20 years | ₹12,00,000 | ₹45–50 lakh |

The first few years look slow…

Then compounding hits like rocket fuel.

If you want to see how your own SIP can grow over the years, try this simple Early Retirement Calculator (India) to estimate your long-term wealth.

Your Monthly Investing Routine

Follow this exact routine:

- SIP date: 1st or 5th

- Use auto-debit

- Increase SIP every year

- Track only once a year

- Don’t stop during market falls

- Stay invested 5–15 years minimum

This is the real formula of how to start investing in India 2025 correctly.

When You Should NOT Invest

You must skip investing if:

- you have high-interest debt

- job is unstable

- emergency fund = zero

- you’re investing only to save tax

- someone promised guaranteed returns

- you don’t understand the product

Fix foundation → then invest.

The Psychology of Successful Investing

Success in investing is about behaviour, not intelligence.

You must understand:

- markets go up & down

- SIPs sometimes show loss

- consistency beats timing

- patience beats predictions

- long-term beats short-term

If you stay rational, you’ll do better than 80% of new investors.

Your First 90-Day Investing Blueprint

Here’s EXACTLY how to start investing in India over the next 3 months:

Month 1

- Build ₹10,000 emergency buffer

- Open Demat

- Start ₹500–₹1,000 SIP

Month 2

- Grow emergency fund

- Increase SIP

- Learn basics

Month 3

- Add PPF/NPS

- Increase SIP again

- Set yearly financial goals

Once you finish 90 days, investing becomes effortless.

FAQs — How to Start Investing in India

Is ₹500 enough to start investing in India?

Yes, perfect for beginners.

Which investment is best for beginners?

Nifty 50 Index Fund.

Should I time the market?

No. SIP removes timing stress.

Is PPF better or NPS?

PPF = safest

NPS = retirement + tax benefits

How long should I invest?

Minimum 5–7 years.

Ideal 10–20 years.

Should beginners buy stocks?

Not in the beginning.

Which app is safest?

Groww, Zerodha, Upstox.

Can I lose money?

Short term: Yes

Long term: Unlikely if disciplined

Conclusion

Learning How to Start Investing in India is not about being perfect — it’s about beginning.

You don’t need big money.

You don’t need expert-level knowledge.

You don’t need to understand every product.

You just need:

- one emergency fund

- one simple index fund

- one SIP

- one clear plan

- and a little patience

Start small.

Stay consistent.

Increase slowly.

Let compounding work silently in the background.

This is the real formula for How to Start Investing in India 2025 — simple, practical, and achievable for every Indian household.

Your future self will thank you.