If you’ve been watching your EPF balance grow — or relying on it as your safety net — the EPF withdrawal rules 2025 have changed the game.

The Employees’ Provident Fund Organisation (EPFO) has approved major updates that redefine how, when, and how much you can withdraw from your provident fund.

This isn’t a small tweak — it’s a complete shift toward a more digital, flexible, and member-friendly system. But like any financial reform, what looks simple on the surface carries deep implications for your money.

Let’s break it all down clearly — what’s new, what it means for you, and how to plan wisely.

EPF Withdrawal Rules 2025 — What Changed

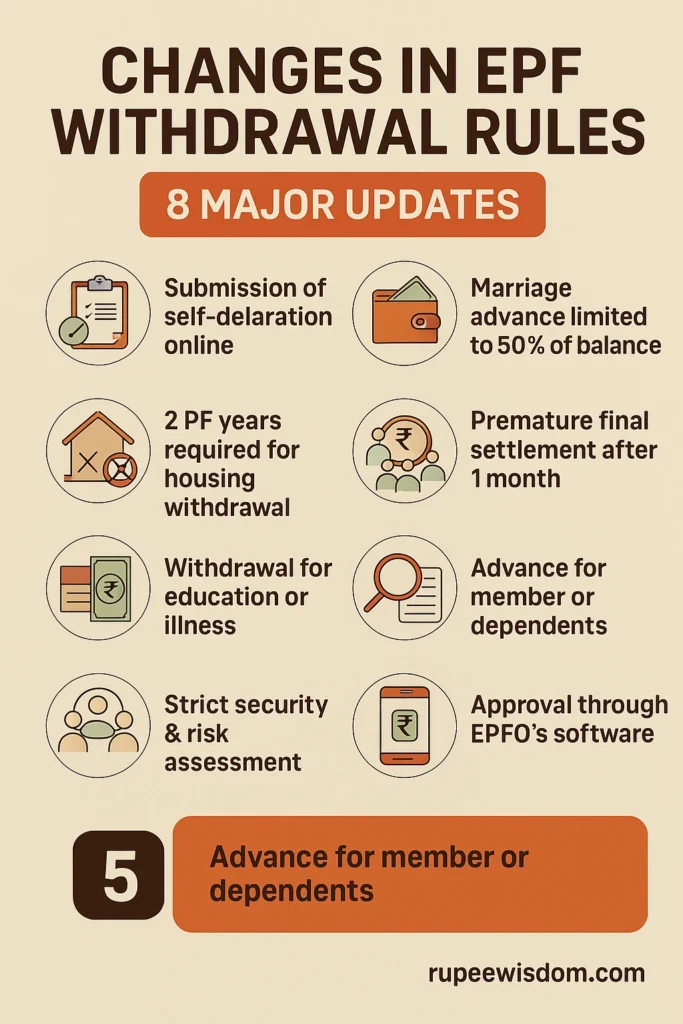

EPFO’s new framework brings eight major changes to simplify and modernize withdrawals. Here’s a quick side-by-side view:

| Change | Old Rule | New Rule 2025 |

|---|---|---|

| Number of withdrawal categories | 13+ specific categories | Merged into 3 broad categories |

| Maximum withdrawal | 50–75% (varied) | Up to 100%, with mandatory minimum balance |

| Minimum service period | 5–7 years | 12 months for most withdrawals |

| Full settlement (after job loss) | 2 months unemployment | 12 months unemployment required |

| Pension withdrawal | 2 months | 36 months waiting period |

| Processing | Manual, employer-dependent | Digital, Aadhaar/PAN-verified auto-settlement |

| Medical/emergency withdrawals | Limited frequency | More frequent, simplified access |

| Grievance & disputes | Slow, paper-heavy | Digital redressal via Vishwas scheme |

These updates are designed to make EPF withdrawals faster, fairer, and easier — while protecting your long-term savings.

For the latest official notifications and circulars, visit the EPFO official website.

What These EPF Changes Mean for You

Here’s what really matters — how these rules affect your life and decisions.

Simplified categories = faster approvals

No more confusion between 13 different withdrawal types.

Now, everything falls into three clear categories:

- Life & essential needs (education, medical, marriage)

- Housing and property

- Special circumstances (unemployment, critical illness, etc.)

Why it matters: You’ll face fewer rejections and less paperwork.

Up to 100% withdrawal allowed (with balance rule)

EPFO is now allowing members to withdraw up to 100% of their balance, provided they maintain a minimum balance (around 25%) for future growth.

Why it matters: You get emergency liquidity without wiping out your retirement corpus.

Be careful: The money you withdraw now loses compound interest forever — use this power sparingly.

Minimum service period reduced to 12 months

Previously, many withdrawals (like housing or education) required 5–7 years of service. Under the new rule, 12 months of continuous service makes you eligible for most withdrawals.

Why it matters: Newer employees can access funds for legitimate needs much earlier.

Full and pension withdrawals now take longer

If you’re unemployed, you’ll have to wait 12 months before a full EPF settlement (previously 2 months). For pension withdrawal, the waiting period has extended to 36 months.

Why it matters: You must plan your cash flow — EPF is no longer a short-term fallback after job loss.

Digital-first processing for all claims

EPFO is moving fully digital — Aadhaar, PAN, and bank verification will drive approvals. Many claims will now be auto-settled, reducing delays and human errors.

Why it matters: Faster payouts, fewer manual interventions, and real-time status tracking.

Action step:

Complete your UAN KYC — link Aadhaar, PAN, and bank account. Keep your mobile and email verified.

Medical, marriage, and education withdrawals — more flexibility

EPFO now allows multiple withdrawals for repeated life events. For example, you can withdraw for multiple education stages or multiple medical needs.

Why it matters: No more one-shot restrictions — real-world flexibility.

But: Each withdrawal still affects your compounding growth.

Auto advances for emergencies

A new auto-claim facility is being expanded. If your KYC and eligibility are complete, the system can automatically trigger payouts for emergencies (like hospitalization or job loss).

Why it matters: You get emergency funds instantly — no waiting for HR approvals.

Faster dispute resolution via Vishwas scheme

The EPFO is launching a “Vishwas” initiative to resolve old claims, cut litigation, and process settlements faster.

Why it matters: Less red tape, fewer delays, and faster resolution if your claim hits a snag.

EPF Withdrawal Rules 2025 in Real Life — Practical Scenarios

Scenario 1: Job loss and loan EMIs piling up

You’ve been unemployed for six months and want to pay off your credit card debt.

- Old rule: Full withdrawal not allowed until 2 months → done quickly

- New rule: Must wait 12 months for full withdrawal, but partial withdrawal is easier and higher

Use partial withdrawal (up to 75%) to clear high-interest loans.

Avoid draining the full corpus — that’s your long-term safety net.

Scenario 2: Buying your first home

Earlier, you needed at least 5 years of service to withdraw EPF for housing. Now, you can do it after 1 year.

Ideal for young professionals.

But withdraw only what’s needed for the down payment — not the full amount.

Scenario 3: Medical emergency

EPFO now allows self-declaration for medical withdrawals. With the new auto-claim feature, funds can hit your account within days if your UAN is KYC-complete.

Keep all hospital records.

Don’t rely on this system without verifying your UAN details first.

Scenario 4: Financial temptation

Withdrawals are now easier — but that’s exactly the danger.

Just because you can doesn’t mean you should.

EPF is designed for financial protection, not spontaneous spending.

EPF Withdrawal Rules 2025 — Decision Framework

Ask yourself these questions before touching your EPF:

- Is this an emergency or high-interest debt?

If not, stop right here. - Will the benefit outweigh the lost interest?

EPF earns ~8% annually. Only withdraw if your debt costs >15–18%. - Can you do a partial withdrawal instead of full?

Always prefer partial — it keeps compounding alive. - Will you rebuild savings afterward?

Plan recovery from withdrawal immediately after stability returns.

Mistakes That Could Cost You

- Using EPF for luxury or vacations

- Assuming old rules still apply

- Filing claims without updated KYC

- Repeated withdrawals destroying compounding

- Ignoring new waiting periods for full settlement

Quick Checklist Before Applying

- 12-month service completed

- KYC done (Aadhaar, PAN, bank linked)

- Valid reason fits into new category

- Verified your current mobile/email in UAN

- Withdrawal amount calculated smartly

- All proofs (bills, receipts) ready for record

- Confirmed new timelines (12/36 months)

EPF Withdrawal vs Loan Example

You have ₹2,00,000 in EPF. You owe ₹1,50,000 on a personal loan at 18% interest.

- EPF earns ~8%.

- Loan costs you ~₹27,000 per year in interest.

- Lost EPF interest = ₹12,000.

- Net saving = ₹15,000.

Withdraw to clear high-interest debt, but only the exact amount.

Don’t empty your account — future compounding is your real wealth.

EPF Withdrawal Rules 2025 — Action Plan

- Finish KYC (Aadhaar, PAN, bank)

- Merge all EPF accounts under one UAN

- Avoid multiple withdrawals

- Use EPF only for emergencies or life goals

- Rebuild contributions post-withdrawal

- Follow official EPFO updates regularly

Frequently Asked Questions (FAQ)

Q1. Can I withdraw 100% EPF under the new rules?

In some conditions, yes — but a mandatory minimum balance applies. Always check your eligibility before filing.

Q2. How long must I be unemployed for full settlement?

Now 12 months of unemployment are required.

Q3. Can I withdraw my pension early?

Pension withdrawals need 36 months of unemployment as per the new framework.

Q4. How fast will I get my withdrawal amount?

Digital processing means faster settlements — sometimes within 3–5 working days, provided your KYC is verified.

Q5. Does withdrawing affect my interest earnings?

Yes. You’ll only earn interest on the remaining balance. Withdraw smartly.

Conclusion

The EPF withdrawal rules 2025 make accessing your savings easier than ever — but that freedom comes with responsibility.

Use it for the right reasons: genuine emergencies, clearing high-interest debt, or achieving life milestones.

If you misuse this easier access, you risk dismantling the very financial safety net meant to protect you.

The smartest Indians won’t rush to withdraw — they’ll plan, calculate, and act only when it truly makes sense.

That’s RupeeWisdom in action.