It’s the 20th of the month. The fridge is full, the wallet is empty, and another “salary finished early” conversation brews at the dinner table.

Sound familiar? You’re not alone. Most Indian families don’t overspend — they underplan. Budgeting isn’t about spreadsheets and sacrifice; it’s about peace of mind. That’s why finding the best budgeting method for Indian households has become a real need today.

It’s making sure rent gets paid, school fees don’t shock you, groceries don’t drain you, and there’s still room to save and breathe. If you find yourself mid-month wondering, “Where did all the money go?” — this guide is for you.

Most financial advice online speaks to individuals, not households. But real India functions as families — where incomes merge, expenses multiply, and priorities collide. You don’t just need a “budget” — you need a budgeting method built for Indian families.

💡 At a Glance: Best Budgeting Method for Indian Families

- ✔️ Learn a practical budgeting method designed for Indian households — not Western templates.

- ✔️ Step-by-step guide with real examples for ₹50,000–₹1 lakh incomes.

- ✔️ Includes family-focused tweaks for EMIs, rent, school fees, and groceries.

- ✔️ Helps you balance saving, spending, and lifestyle peacefully.

- ✔️ Easy to implement — no complex spreadsheets, just structure and discipline.

And if you’re looking for the best budgeting method for Indian families, this guide will help you structure your money in a way that actually works for real Indian households.

- Why family budgeting is different

- The single best budgeting method for Indian families

- Step-by-step implementation with real Indian examples

- Practical tweaks for EMIs, kids, and parents

- Common mistakes and how to fix them

- Tools you can use right away

Let’s dive in.

Why Family Budgeting Must Be Different

Family life brings beautiful chaos—and complex finances. When more than one person depends on the same income stream, you can’t use a one-size-fits-all plan.

Here’s why family budgeting must work differently:

1. Fixed commitments grow fast.

Rent, EMIs, groceries, utilities, insurance, parents’ medical costs—these aren’t optional. “Needs” can easily cross 60% of total income.

2. Discretionary spending multiplies.

Weekend dining, kids’ gadgets, gifts, and spontaneous holidays—all these quietly bleed cash if you don’t set limits.

3. Incomes fluctuate.

If one spouse has variable pay, or a business income drops, it shakes the entire setup. Flexibility is key.

4. Shared goals matter.

You’re not just saving for yourself anymore. You’re saving for education, retirement, and stability.

That’s why the usual “50/30/20” formula often fails real Indian families. It’s too rigid for our mixed-income, high-commitment lives.

The best budgeting method for Indian families must adapt to diverse incomes, shared expenses, and emotional priorities that shape real Indian homes.

You need something more adaptable, transparent, and family-friendly.

The Best Budgeting Method for Indian Families

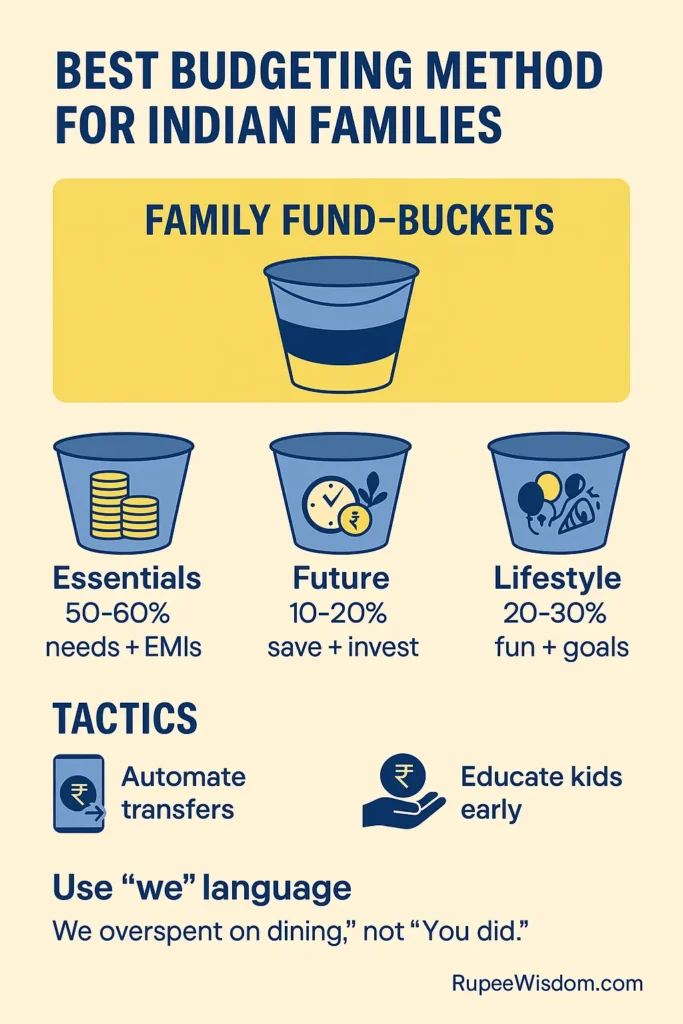

Here’s what truly works — the best budgeting method for Indian families, also known as the Family Fund-Buckets Method.

The Family Fund-Buckets Method

It’s a modern, Indian adaptation of the 50/30/20 model — structured for real-life family situations.

It’s simple to apply, easy to maintain, and creates harmony by assigning a purpose to every rupee.

Family Budget Example: ₹1 Lakh Monthly Income

Let’s say your family earns ₹1,00,000 per month.

Here’s how a balanced, realistic Indian budget might look when you apply this method:

₹1 Lakh Family Budget Breakdown (Real-Life Example)

| Category | % of Income | Example (₹) | Key Expenses |

|---|---|---|---|

| Essentials | 55% | ₹55,000 | Rent, EMIs, groceries, utilities, school fees |

| Savings & Future Goals | 20% | ₹20,000 | SIPs, insurance, emergency fund, child’s education |

| Lifestyle (Wants) | 15% | ₹15,000 | Dining out, OTT, shopping, family outings |

| Buffer / Flex Fund | 10% | ₹10,000 | Unexpected expenses or short-term goals |

👉 If your rent or EMIs are high, shift temporarily to a 60/20/10/10 model — just ensure at least 15–20% of your income still goes toward future goals.

The Structure

| Bucket | Purpose | Recommended % of Total Income |

|---|---|---|

| Essentials (Fixed + Variable Needs) | Rent, EMIs, groceries, utilities, insurance, school fees | 50–60% |

| Safety & Future | Emergency fund, debt repayment, SIPs, health cover | 15–20% |

| Family Goals & Experiences | Vacations, gifts, upgrades, kids’ activities | 10–15% |

| Lifestyle / Discretionary | Dining out, OTT, shopping, comfort spends | 5–10% |

Why This Method Works

- It prioritizes peace. Essentials come first, so survival isn’t stressful.

- It protects your future. The Safety bucket ensures you’re saving and repaying debt before spending on extras.

- It respects emotion. Families need celebration and joy—this plan makes room for that without guilt.

- It keeps you flexible. If one income dips, you can trim Lifestyle and Goals without touching Safety.

- That balance and adaptability are what make this system the best budgeting method for Indian families living across metros and smaller cities alike.

How to Apply the Family Fund-Buckets Method

- Calculate your total net income.

Combine all household incomes after taxes. Don’t guess—check your actual credit entries. - List all fixed commitments.

Rent, EMIs, school fees, insurance, and utilities. These form your non-negotiables. - Estimate variable needs.

Groceries, transport, household help, and medical needs. - Allocate Essentials first.

If they cross 60%, tighten Lifestyle temporarily until you regain balance. - Automate Safety & Future.

On salary day, auto-transfer a fixed amount to an emergency fund or investment account. Treat it like another bill. - Create Sinking Funds for Big Goals.

For school fees, vacations, or car upgrades — divide the total by 12 and auto-save monthly. - Decide your Lifestyle allowance.

Keep this visible and finite—when it’s gone, it’s gone. That’s how you build spending discipline. - Hold a Monthly Family Review.

Sit down for 15 minutes each month. Review spends, celebrate savings wins, and set next month’s priorities.

Rules to Keep It Running Smoothly

- Automate savings on salary day — don’t rely on memory or willpower.

- Track expenses weekly, not monthly. Small leaks are easier to plug early.

- Pause Lifestyle spending if you miss your Safety target for two months in a row.

- Keep transparency: every family member knows where money goes.

Practical Tweaks for Different Indian Families

High-Rent Cities (Mumbai, Delhi, Bengaluru)

Rent may touch 30–35% of income. Let Essentials rise to 65% temporarily, but cap Lifestyle at 3–5%. Keep Safety steady at 20%. Review every 6 months.

Two-Income Homes with One Variable Earner

Use your lowest predictable combined income as your base. Treat any surplus as bonus and route it directly to Safety or Goals. Never plan budgets on “expected” variable pay.

These small but powerful tweaks are what make the best budgeting method for Indian families sustainable in the long run, regardless of lifestyle or income range.

Families with Kids and School Fees

Start a dedicated School Fees Fund. Divide annual fees by 12 and automate deposits. No more “fee shock” months.

Supporting Elderly Parents

Classify parental support under Essentials. Add a small medical reserve to the Safety bucket—say ₹1,000–₹2,000 per month—for sudden needs.

Side-Hustle Income or Bonuses

Don’t mix it with your monthly cash flow. 70% goes straight into Safety, 30% into Goals. Avoid lifestyle creep.

Common Budget Mistakes Indian Families Make

1. No unified tracking.

Each spouse or member spends independently, no one knows the total.

→ Fix: Use a shared Google Sheet or family expense app. Transparency builds trust.

2. Thinking income will keep growing.

Families assume future hikes will fix poor discipline.

→ Fix: Budget for the present. Upgrade Lifestyle only when savings ratio improves.

3. Treating savings as “whatever’s left.”

That’s why there’s never anything left.

→ Fix: Flip the flow. Save first, spend what remains.

4. Over-splitting responsibilities.

One spouse handles EMIs, another savings—no coordination.

→ Fix: Pool income for Essentials + Safety. Keep Lifestyle separate if needed, but plan jointly.

5. Ignoring inflation and irregular expenses.

Annual insurance premiums, school fees, or festival costs break monthly rhythm.

→ Fix: Create 3–5 small “sinking funds” for such costs. Contribute monthly.

6. Budget once, then forget.

A budget is a living system, not a one-time chart. That’s exactly why the best budgeting method for Indian families focuses on flexibility, regular reviews, and shared accountability instead of rigid spreadsheets.

→ Fix: Review monthly. Adjust percentages with reality, not pride.

Tools You Can Start Using Tonight

- Two bank accounts:

- Account 1 → Essentials + Safety

- Account 2 → Goals + Lifestyle

Automate transfers on salary day.

- Free trackers: Walnut, Money View, or Google Sheets.

Track by categories, not by chaos. - Visual reminders:

Print your bucket table on the fridge or family WhatsApp group. When everyone sees it, spending decisions change. These visual and digital habits form a core part of the best budgeting method for Indian families, helping every member stay mindful and aligned. - Calendar rule:

On the 28th of each month, hold your “Family Money Meet.” 15 minutes, one goal—stay on plan.

Advanced Family Budgeting Tips

1. Build a mini-buffer.

Always keep 5% of income as a “misc” buffer. This covers forgotten payments, birthday gifts, or surprise guests.

2. Assign roles.

Let one partner handle tracking, another automation. Shared accountability prevents burnout.

3. Don’t hide purchases.

Secret expenses destroy both the budget and trust. Bring all financial activity to the table.

4. Upgrade your buckets annually.

Every 12 months, review all percentages. As income rises, boost Safety and Goals before Lifestyle. Regular reviews ensure even the best budgeting method for Indian families stays relevant as costs, goals, and responsibilities evolve.

5. Reward progress.

When your family hits a goal (like ₹1 lakh emergency fund), celebrate. Budgeting should feel empowering, not punishing.

Mini Budget Templates for Quick Start

Template 1: ₹60,000 Joint Income (One Child, Tier-2 City)

- Essentials: ₹35,000

- Safety & Future: ₹10,000

- Goals & Experiences: ₹8,000

- Lifestyle: ₹4,000

- Buffer: ₹3,000

Template 2: ₹1,20,000 Joint Income (Metro City, Two Earners)

- Essentials: ₹65,000

- Safety & Future: ₹25,000

- Goals & Experiences: ₹18,000

- Lifestyle: ₹10,000

- Buffer: ₹2,000

Adjust numbers, not purpose. The bucket logic stays universal.

How to Turn Budgeting into a Family Habit

- Make it visible. Post your monthly plan somewhere the family sees it.

- Keep meetings short. 15 minutes. No lectures, no guilt trips—just numbers.

- Celebrate wins. Saved ₹5,000 this month? Family treat within the Lifestyle bucket.

- Educate kids early. Give small spending envelopes, teach tracking.

- Use “we” language. “We overspent on dining,” not “You did.” Keeps unity alive.

Related Reading

Start with one simple change — automate savings on salary day. It’s the habit that transforms every budgeting method from theory to success. Once your family sees progress, you’ll never go back to chaos.

Conclusion

Budgeting for Indian families isn’t about cutting joy—it’s about creating peace.

The Family Fund-Buckets Method helps you do exactly that: it keeps your essentials secure, your future protected, and your lifestyle controlled.

Start this month. Calculate your income, set your buckets, automate transfers, and review together. Within 90 days, you’ll feel calmer, more confident, and in charge of your money instead of at its mercy.

Because the best budgeting method for Indian families isn’t about sacrifice—it’s about structure.

When your family works with a system, money becomes a tool for living better, not just surviving longer.