How to make a monthly budget in India is one of the most important personal finance skills you can learn in 2025.

If you’ve ever looked at your bank balance mid-month and thought, “Where did my salary disappear?” — you’re not alone.

Between rent, EMIs, groceries, and random weekend expenses, most people run out of money before the month ends.

This guide will teach you exactly how to make a monthly budget in India — practical, realistic, and designed for Indian salaries and expenses.

Why You Must Learn How to Make a Monthly Budget in India

In India, budgeting is not just about saving money — it’s about survival.

Everything costs more each year: rent, petrol, food, tuition, even data plans.

Without a budget, you don’t realize how quickly income leaks out through small, daily spends.

A monthly budget helps you:

- Know where every rupee goes

- Plan savings automatically

- Prevent debt and loan dependency

- Build discipline and financial security

Budgeting gives you clarity — and that’s the first step toward financial freedom.

(For official money management principles, the Reserve Bank of India’s Financial Education portal is an excellent resource to explore.)

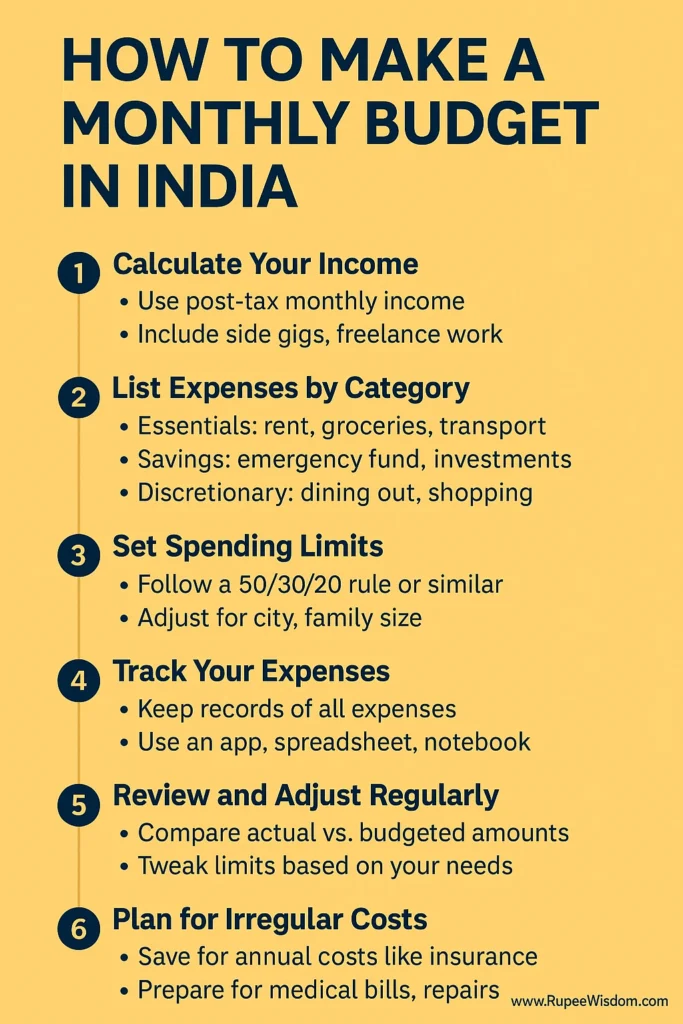

Step 1: Calculate Your Real Take-Home Salary

The first step in learning how to make a monthly budget in India is knowing your true income.

Most people confuse CTC with income. It’s not.

Use your actual take-home pay — the amount credited after taxes, PF, and deductions.

If you earn variable income (commissions or freelance), take the average of the last three months and base your plan on the lowest one.

Add consistent side income only if it’s guaranteed every month.

Your budget is only as real as your numbers.

Step 2: List Every Expense Before You Budget

Before you can create a monthly budget, you need to know where your money goes.

List your expenses in three parts:

1. Fixed Essentials

Rent, school fees, insurance, EMIs, and transport passes — these don’t change much.

2. Variable Costs

Groceries, dining out, OTT, shopping, and personal spending. These change monthly but must be capped.

3. Hidden or Irregular Expenses

Festivals, annual bills, and repairs. Divide these by 12 and add them to your monthly plan.

Tracking expenses for one full month will show you patterns you never noticed — it’s the eye-opener that powers every smart budget.

Step 3: Choose a Budgeting Rule That Suits India

To understand how to make a monthly budget in India effectively, you need a budgeting framework.

The world loves the 50/30/20 rule, but in India, it often needs tweaking.

Option 1: The 50/30/20 Rule

- 50% on Needs (rent, groceries, transport, EMIs)

- 30% on Wants (leisure, shopping, outings)

- 20% on Savings and Investments

Option 2: The India-Tuned 55/15/20/10 Rule

- 55% for Essentials

- 15% for EMIs and debt

- 20% for Savings and Safety

- 10% for Lifestyle

Why this matters: Indian expenses are rent-heavy. This version is realistic and still leaves room for savings.

Step 4: Build Your Monthly Budget Template

Now let’s apply it practically.

Example: ₹50,000 Take-Home Salary

| Category | Percentage | Amount (₹) | Purpose |

|---|---|---|---|

| Essentials | 55% | 27,500 | Rent, groceries, transport, bills |

| Debt/EMIs | 15% | 7,500 | Loan or card payments |

| Savings & Safety | 20% | 10,000 | Emergency fund + insurance |

| Lifestyle | 10% | 5,000 | Dining, OTT, personal treats |

Here’s how to implement it:

- Transfer savings (₹10,000) the same day salary hits.

- Use your main account for bills and EMIs.

- Keep lifestyle spending separate in cash or a prepaid card.

- Check progress weekly.

This is how to make a monthly budget in India that’s simple and sustainable — no spreadsheets needed.

Step 5: Automate Your Budget for Success

Automation is the secret behind every consistent budgeter.

Once you set automatic transfers and payments, the system runs itself.

- Set auto-transfer of 20% to your savings account

- Schedule EMIs and SIPs through net banking

- Use recurring deposits for short-term goals

- Keep different UPI IDs for bills and personal spending

The less manual control you need, the more successful your budget will be.

Step 6: Review and Adjust Monthly

A good monthly budget in India is flexible, not rigid.

At the end of every month:

- Compare budgeted vs actual spending

- Identify which category overflowed

- Adjust limits for the next month

- Move leftover money to your emergency fund

Think of it like a health check-up for your wallet.

Budgets evolve as your life changes — promotions, rent hikes, or new goals.

Step 7: Add India-Specific Tweaks

When you’re learning how to make a monthly budget in India, adapt it to local realities.

Rent and City Tier

In metros, cap rent at 30% of income.

If you live with family or in Tier-2 cities, redirect that savings into insurance or mutual funds.

EMI Management

Keep EMIs below 20% of your salary.

If they exceed this, focus on a 3-month “debt sprint” — cut luxury spending and close one loan early.

Emergency Fund

Target at least two months of expenses saved in a separate account.

Start small — ₹2,000–₹3,000 a month — and grow gradually.

Festival and Family Costs

Plan ahead for Diwali, weddings, or school fees by saving monthly in a “Sinking Fund.”

Side Income

Use bonuses or freelance money only for savings or investments, not for lifestyle inflation.

Step 8: Sample Budgets by Income Level

Example A: ₹30,000 Income

- Essentials: ₹16,500

- Debt: ₹4,500

- Savings: ₹6,000

- Lifestyle: ₹3,000

Goal: build an emergency fund and avoid new loans.

Example B: ₹50,000 Income

- Essentials: ₹27,500

- Debt: ₹7,500

- Savings: ₹10,000

- Lifestyle: ₹5,000

Goal: balance savings, insurance, and some comfort.

Example C: ₹1,00,000 Income

- Essentials: ₹50,000

- Debt: ₹10,000

- Savings: ₹25,000

- Lifestyle: ₹15,000

Goal: shift focus to investments and early financial independence.

Each model shows you how to make a monthly budget in India that matches your lifestyle and income bracket.

Step 9: Build Discipline and Stick With It

A perfect budget is useless if you don’t follow it.

Consistency is everything. Here’s how to make your monthly budget stick:

- Save before you spend — automate it.

- Track expenses weekly, not at month-end.

- Use a separate wallet or card for discretionary spends.

- Have one “no-spend” day every week.

- Celebrate small wins like hitting a savings target or closing a debt.

Habits keep you financially grounded even when life gets unpredictable.

Step 10: How Budgeting Helps Avoid Debt Traps

This is where budgeting becomes life-changing.

Most debt problems start with small oversights — missed EMIs, card bills, or impulse buys.

A monthly budget prevents this spiral.

It helps you:

- Spot cash flow problems early

- Manage EMI load properly

- Negotiate confidently if settlement ever becomes necessary

- Build real savings that replace credit dependency

When you understand how to make a monthly budget in India, you gain not just savings — you gain stability.

Common Mistakes to Avoid

| Mistake | Why It Happens | How to Fix It |

|---|---|---|

| Budgeting from memory | You “guess” expenses | Track every rupee for a month |

| Saving last | You wait for leftover cash | Save first, spend later |

| Ignoring small leaks | You think ₹100 doesn’t matter | Add them up — they do |

| Leaving EMIs out | You treat them as automatic | Always include them in expenses |

| Never reviewing | You assume it’s fixed | Review and update monthly |

Avoiding these mistakes is the difference between a working plan and a forgotten spreadsheet.

Frequently Asked Questions on Monthly Budgeting in India

Q1: What if my income isn’t fixed every month?

Base your plan on the lowest recent income and treat extra earnings as bonus savings.

Q2: Should I start investing before an emergency fund?

No. Build at least 2 months of emergency cash first — then invest.

Q3: My rent is too high. Should I move?

If rent exceeds 35% of your income, yes. Shared accommodation or relocation can transform your savings.

Q4: Do I need a budgeting app?

Not really. A notebook or Google Sheet works perfectly — the key is consistency.

Q5: What if I overspend every month?

Reduce your “wants” by 10% and start tracking weekly. Progress beats perfection.

The 30-Minute Monthly Budget Routine

On Salary Day

- Transfer 20% to savings.

- Pay EMIs and rent.

- Keep essentials fund ready.

- Allocate lifestyle cash separately.

- Log your plan.

Mid-Month

Check progress and adjust.

Month-End

Move leftovers into savings or investments.

Repeat next month. The system strengthens itself.

Conclusion: Build Freedom with a Real Indian Budget

Now you know exactly how to make a monthly budget in India that actually works.

It’s not about sacrifice — it’s about structure.

Once your budget is set, your money finally listens to you instead of the other way around.

Start small. Track one month.

Within 90 days, you’ll have savings, stability, and peace of mind — all from a few simple habits.

Financial freedom doesn’t begin with a raise.

It begins with clarity, control, and a consistent monthly budget.