You can plan your investments, compare mutual funds, or dream about early retirement —

but one unexpected medical bill or job loss can wipe that dream clean in days.

That’s where your emergency fund steps in — your personal financial bodyguard.

Before you even think about investments or SIPs, learning how to save for emergency fund in India gives you the foundation for everything else.

If you’ve been wondering how to save for emergency fund in India — when expenses already eat most of your salary — this guide is exactly what you need.

No jargon. No theory.

Just a practical, step-by-step Indian approach to building a safety net that actually protects you — not your bank manager.

You’ll learn how much to save, where to keep it, and the habits that make it grow quietly in the background while you live your life stress-free.

Let’s start where it matters most — your first rupee.

Learning how to save for emergency fund in India is the first step to financial freedom — because without it, even the best investments fall apart.

Why Saving for an Emergency Fund Matters

Without a cushion, you might fall back on high-interest loans, miss investment opportunities, or face serious stress.

In India, where income can fluctuate, medical costs rise fast, and family responsibilities expand overnight, an emergency fund isn’t a luxury — it’s survival armor.

A proper fund keeps your long-term goals intact even during short-term chaos.

Before you decide where to keep your money, it’s essential to understand how to save for emergency fund in India step-by-step, especially if you’re managing expenses on a tight income.

Imagine this: you lose your job tomorrow. Bills, rent, EMIs, and groceries still keep rolling in.

If you have an emergency fund worth 6 months of expenses, you’re calm, composed, and in control.

If not — panic becomes your financial plan.

How Much Should You Aim to Save?

The golden rule: 3–6 months of essential expenses.

If your income is unstable (freelancer, gig worker, or business owner) or you have dependents, target 6–12 months.

💡 Pro Tip: Use the RBI Financial Education – Money Kumar Series for foundational resources and tools that support your plan on how to save for emergency fund in India.

Quick Indian Example

- Single earner, ₹50,000/month expenses: Save ₹1.5–3 lakh.

- Dual-income couple with ₹80,000/month expenses: Save ₹2.4–4.8 lakh.

- Self-employed or commission-based income: Save ₹5 lakh+.

Keep it simple: start small, but stay consistent. Even ₹3,000/month matters when done steadily.

Your emergency fund covers essentials only — rent, groceries, EMIs, utilities, insurance, school fees — not luxuries like Netflix, travel, or gadgets.

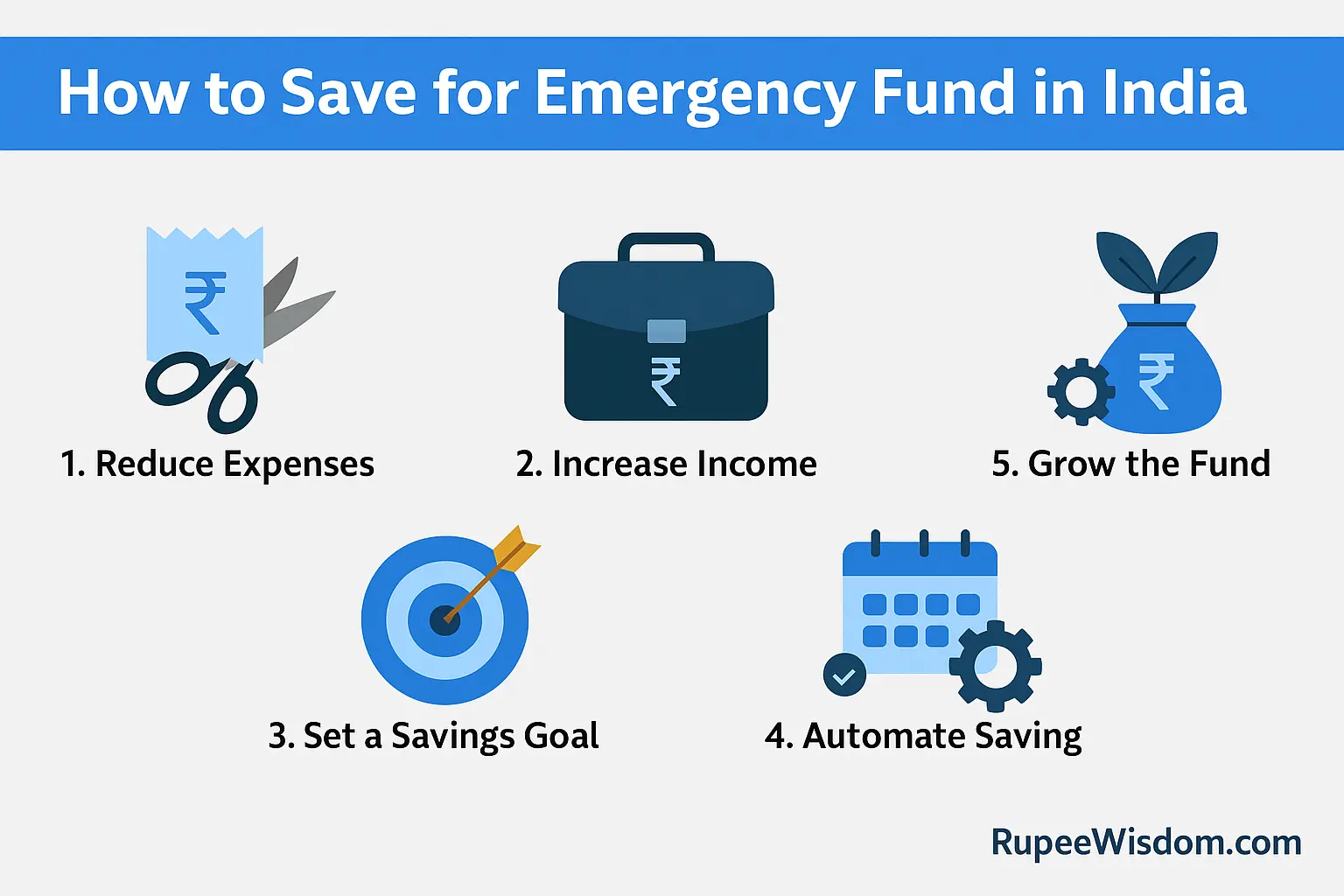

Step-by-Step: How to Save for Emergency Fund

Here’s your clear, India-specific roadmap on how to save for emergency fund effectively — even if you’re just starting from zero.

1. Set a Clear Target and Timeline

Write down your essential monthly expenses.

Now decide how many months of coverage you want (3, 6, or 12).

Then multiply and fix that number as your target.

Example:

Monthly expenses = ₹40,000

Target = ₹40,000 × 6 = ₹2.4 lakh

Now, give yourself a deadline. For instance, “I’ll save ₹10,000/month to reach ₹2.4 lakh in 24 months.”

Once you attach numbers and dates, it stops being a dream and becomes a plan.

2. Automate Your Savings

The less you handle it, the more likely you’ll stick to it.

- Set up standing instructions from your salary account to a separate “Emergency Fund” account on salary day.

- Redirect windfalls (bonus, tax refund, incentives) directly into the fund.

- Treat it as a non-negotiable bill.

Set it up once and forget it. When saving becomes automatic, it stops being optional.

3. Trim, Redirect, and Simplify

Most people think they can’t save — but small leaks sink big ships.

Track your monthly spending for 30 days.

You’ll find at least ₹2,000–₹5,000 to free up from things like:

- Over-ordering food

- Streaming subscriptions you rarely use

- Impulse online shopping

- Idle memberships

Cut one or two habits and redirect the same amount to your emergency fund.

It’s not about deprivation — it’s about redirection.

When you finish an EMI or clear a loan, keep paying that same amount — just to yourself this time.

4. Use Side Income and Windfalls

Don’t underestimate bonuses, freelance gigs, Diwali gifts, or cashback rewards.

Every extra rupee is an opportunity.

Follow a simple rule:

50% of all unexpected income → Emergency Fund.

You’ll reach your goal far quicker without feeling the pinch in daily life.

This also turns saving into a small celebration of progress — not sacrifice.

5. Break It Into Milestones

Large goals feel heavy; small ones feel achievable.

Think of your fund as stages, not one big mountain:

| Milestone | Time Frame | Corpus Goal | Feeling |

|---|---|---|---|

| Level 1 | 3 months | 1 month’s expenses | First win 🎯 |

| Level 2 | 6 months | 3 months’ expenses | Confidence ✅ |

| Level 3 | 12 months | Full target achieved | Freedom 💪 |

Celebrate each milestone — not by spending, but by acknowledging progress.

Consistency is sexier than intensity in personal finance.

6. Create a Dedicated Account

Never mix your emergency fund with your regular account.

Open a new savings account, or set up an auto-sweep FD linked to it.

Label it clearly — “Family Safety Fund” or “Plan B Account.”

That emotional naming creates mental resistance to dipping into it for trivial reasons.

Avoid investing this fund in risky or long-term instruments. Liquidity is key.

7. Review and Rebalance Each Year

Inflation, EMIs, family size, and salary — everything changes annually.

Your fund must evolve with you.

Do a quick review every 12 months:

- Has your expense pattern changed?

- Do you have new responsibilities (child, home loan, parents)?

- Is inflation eating into your coverage?

If yes, adjust your target upward.

Think of your emergency fund as a living system — it needs maintenance, not just creation.

Budgeting Hacks to Build It Faster

If you’re figuring out how to save for emergency fund in India faster, these budgeting hacks can shave months off your timeline.

- Follow 50/30/20 or 50/20/30 rule.

- 50% essentials

- 20–30% savings

- 20–30% lifestyle

Temporarily shift extra 10% toward your emergency fund until goal completion.

- Automate transfers.

Use standing instructions via your bank or UPI autopay. Automation = consistency. - Stay under DICGC limit.

Keep deposits below ₹5 lakh per bank for safety insurance coverage. - Set monthly challenges.

Try “no Swiggy for 30 days” or “no shopping month.” Redirect every saved rupee to your fund. - Leverage cashbacks and rewards.

Redeem rewards for bills or essentials — then move that cash equivalent into your fund. - Micro-save daily.

Save ₹100/day → ₹3,000/month → ₹36,000/year.

Automate it. You won’t feel it leaving, but you’ll feel the result.

Mistakes to Avoid

- Treating credit cards as emergency funds.

They’re expensive loans, not backups. - Investing emergency money in risky assets.

Stocks and crypto fluctuate. When you need cash, markets crash. - Using the fund for non-emergencies.

Birthdays, weddings, or holidays don’t qualify. - Ignoring inflation.

₹2 lakh saved three years ago won’t buy what it did then. - Not refilling after using it.

If you withdraw, rebuild immediately — this fund must stay whole.

How Long Will It Take?

| Monthly Income | Monthly Savings | Time to Build 6-Month Fund |

|---|---|---|

| ₹50,000 | ₹5,000 | 20 months |

| ₹80,000 | ₹8,000 | 15 months |

| ₹1,00,000 | ₹10,000 | 12 months |

| ₹1,50,000 | ₹15,000 | 10 months |

Start small, stay consistent.

Your fund grows silently — and one day, you’ll realize you built your own financial shock absorber.

Behavioral Tricks That Actually Work

Most people know they should build one, but few truly learn how to save for emergency fund in India the right way — with psychology, not pressure.

- Name your fund: “Family Safety Account” — emotional anchors work better than spreadsheets.

- Visualize progress: Track on Google Sheets or any budgeting app.

- Treat it like a bill: Pay it the moment your salary hits.

- Make it public: Tell your spouse or sibling. Accountability keeps you consistent.

- Automate everything: You can’t fail a system that runs itself.

Tiny changes in behavior turn saving from “should do” into “done.”

<div class=”cta-box” style=”background:#f4f6f8;padding:15px;border-radius:10px;margin:20px 0;”> 💬 Need help building your emergency fund strategy? Our experts guide you through <strong>how to save for emergency fund in India</strong> step by step — no guesswork, no confusion. Start your personalized plan with <strong>Sharma Debt Solutions™</strong> today. </div>

What to Do Once You Reach Your Target

Congrats — you’ve reached your goal! Now protect it smartly.

- Keep it liquid.

You should access it within 24 hours, max. - Diversify slightly for better yield.

Divide your fund:- 40% in savings account (instant access)

- 40% in liquid fund or sweep FD (higher return, still liquid)

- 20% in ultra-short fund or T-Bills (for stability)

- Review once a year.

Adjust for inflation or lifestyle changes. - Rebuild after use.

Anytime you withdraw, restart monthly contributions immediately. - Next step:

Once your safety net is strong, focus on debt repayment or long-term investing.

📖 Related Reading

-

Where to Park Emergency Fund in India (Safest & Smartest Options)

– Your pillar guide to choosing the best places to store your emergency fund safely. -

What Is an Emergency Fund and Why You Need One

– Learn the basics before you start building your fund step-by-step.

Frequently Asked Questions

Here are some of the most common questions people ask when starting their journey on how to save for emergency fund in India.

1. What if I can’t save much?

Start small. ₹1,000/month is fine. The habit is more powerful than the amount.

2. Should I invest my emergency fund?

Only in safe, short-term instruments — savings account, sweep FD, or liquid mutual funds. No equities.

3. When can I use it?

Only during genuine, unpredictable emergencies: job loss, health issues, urgent family crises.

4. How often should I review it?

At least once a year or after major life changes — marriage, home purchase, or childbirth.

5. Can I merge it with other goals?

No. Keep it independent. Travel, gadgets, or weddings should have their own savings buckets.

6. Should I keep it in one bank?

Preferably not beyond ₹5 lakh per bank (for DICGC coverage). Diversify if larger.

Conclusion: Build Your Fund, Build Your Peace

Saving for an emergency fund isn’t about being paranoid — it’s about being prepared.

It’s the foundation that keeps your goals from collapsing when life turns unpredictable.

Start with what you can — even ₹1,000 a month. Automate it. Forget it.

Before you know it, you’ll have built something that feels less like “savings” and more like peace of mind.

If you’ve been postponing it, now’s the time to act — start small, stay consistent, and master how to save for emergency fund in India before chasing any high-return investments.

And once your fund is ready, don’t let it sit idle — learn where to park your emergency fund in India to keep it safe and inflation-proof.

Remember: every strong financial plan begins with one thing — security first, returns later.

Build your emergency fund now. The future version of you will thank you for it.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered financial advice. Readers are encouraged to consult a qualified financial advisor before making investment or money-related decisions. RupeeWisdom.com is not responsible for any financial losses incurred based on the information provided here.