What Happens If You Miss a Credit Card Payment — it may sound small, like “just one day late,” but in the credit world, it can trigger a series of costly consequences and can create ripple effects that hit your wallet, your credit score, and even your peace of mind.

Understanding what happens if you miss a credit card payment early helps you protect your credit score and avoid unnecessary penalties.

What Happens If You Miss a Credit Card Payment in India

So, what happens if you miss a credit card payment in India isn’t just about a late fee — it’s about how banks record your behaviour and how that affects future loans.

When we say miss a credit card payment, it usually means you haven’t paid at least the “minimum due” by the due date shown on your monthly statement.

You might think paying one or two days later is harmless — but technically, it’s already “late.” Every card issuer in India treats it differently, but generally, once your due date passes, the penalties start ticking.

The Minimum Due Trap

Your “minimum due” is the smallest amount required to keep your account active and avoid a default label. Paying only this amount prevents your account from being reported as missed, but not from accumulating interest.

If you pay less than the minimum due — or not at all — it’s counted as missed payment right away.

The Grace Period: Your First Checkpoint

Most banks offer a grace period — a small buffer of a few days after your due date before penalties kick in.

This grace period is usually between 0–3 days, depending on the bank.

If you clear dues during this time:

- Late payment fees may be waived.

- Your next month’s interest-free period may remain intact.

But once you cross that window, interest starts to compound daily on the entire outstanding balance, not just the unpaid part.

So, even a delay of 3–5 days can cost you hundreds or even thousands depending on your balance.

Many people discover what happens if you miss a credit card payment only after losing their interest-free period — and by then, the damage has already started.

Immediate Consequences: Late Fees, Interest & Penalties

Missing your due date has instant financial effects. Let’s break them down.

To really grasp what happens if you miss a credit card payment, let’s look at how your bank reacts from Day 1.

1. Late Payment Fee

Banks charge a flat penalty based on your total outstanding — typically ₹100 to ₹1,000.

The higher your unpaid amount, the bigger the late fee.

For example:

- ₹1,000–₹5,000 outstanding → ₹400 late fee

- ₹5,001–₹10,000 outstanding → ₹750 late fee

- ₹10,001+ outstanding → ₹950–₹1,000 late fee

This charge appears on your next statement — and yes, GST applies on top of it.

2. Interest Rate Spike

When you miss a payment, your card issuer starts charging interest on the full outstanding, not just the unpaid part.

Interest rates for credit cards in India usually range between 3% to 4% per month (36%–48% annually).

Missed payments often trigger penalty interest, which may be higher.

So, if you owed ₹30,000 and didn’t pay, that’s roughly ₹1,200 in interest per month, on top of your late fees.

3. Loss of Interest-Free Period

Normally, you enjoy 45–50 days of interest-free use. Once you miss a payment, this benefit vanishes for the next billing cycles.

Even new purchases start accruing interest from Day 1.

Medium-Term Consequences: Credit Score, Limits & Bank Trust

By this point, you’ll start feeling what happens if you miss a credit card payment for over a month — the penalties begin showing up on your credit report.

If your payment stays overdue beyond a few weeks, the damage deepens.

1. Impact on Credit Score

After 30 days of non-payment, your card issuer reports your account as “late” to credit bureaus like CIBIL, Experian, or CRIF.

One missed payment can drop your credit score by 50–100 points, depending on your history.

That single red mark stays visible for up to 7 years on your report, even if you later pay off the dues.

2. Reduction in Credit Limit

If you repeatedly pay late or skip payments, banks may lower your credit limit.

Why? Because it signals “high-risk borrower.”

You’ll suddenly find your ₹1L limit reduced to ₹50K — which also hurts your credit utilization ratio.

3. Temporary Account Suspension

After two or more missed cycles, your card may be blocked for further transactions. You won’t be able to swipe or use it for online payments until dues are cleared.

Long-Term Consequences: Defaults, Recovery & Legal Issues

If you still wonder what happens if you miss a credit card payment for 90 days or more, here’s how quickly it escalates.

If the dues remain unpaid beyond 90 days, the problem stops being “financial” and starts becoming “legal.”

1. Default Status

After 90–180 days of missed payment, your account is officially marked as default.

This means the bank assumes you’re not going to pay voluntarily.

They’ll stop issuing statements and begin recovery proceedings.

2. Recovery Agents

The bank may hand your account to recovery agencies.

Expect phone calls, messages, and possibly home visits.

If they overstep — threatening or harassing — you can complain to your bank and even escalate it to the RBI Ombudsman under the RBI’s Fair Practices Code for Credit Card recovery

3. Legal Action

If recovery fails, the bank may file a civil case to recover dues.

You won’t go to jail for credit card default alone, but legal proceedings can lead to:

- Asset attachment (if the court allows)

- Civil judgments that hurt your future loan eligibility

- Long-term negative mark on your CIBIL

4. Long-Term Credit Damage

Even after clearing the balance later, the “default” tag remains visible on your credit history for several years.

You’ll need consistent, perfect payments for at least 12–18 months to rebuild trust.

Step-by-Step: What to Do If You Miss a Credit Card Payment

Don’t panic — what happens if you miss a credit card payment isn’t the end of the world if you act fast.

Don’t panic — missing a payment once isn’t the end of the world.

Here’s what you should do immediately to control the damage.

Step 1: Pay Right Away

Even if it’s just a part of your total bill, pay something immediately.

Partial payment reduces interest and might save your credit score from a 30-day report.

Step 2: Call Your Card Issuer

Explain the situation — illness, emergency, system delay — and politely request a late fee waiver.

If it’s your first slip, most banks will remove it as goodwill.

Step 3: Convert Dues to EMI

If you can’t pay full, ask for EMI conversion.

This changes your balance into smaller monthly installments with manageable interest (1–1.5% per month instead of 3–4%).

Step 4: Avoid Using the Card Until You’re Current

New swipes after missing a payment only add to your interest pile.

Pause usage until dues are cleared.

Step 5: Check Your Credit Report

After paying, check your CIBIL or Experian report in 30–45 days.

Ensure your late payment isn’t wrongly reported as default. If it is, raise a dispute online.

Prevention Techniques: How to Never Miss a Payment Again

The best fix is prevention. Here are real-world ways to make sure you never fall behind again.

1. Set Auto-Pay for Full Amount

Enable auto-debit for full payment from your savings account every month.

Avoid setting auto-pay to “minimum due” — that only delays interest buildup.

2. Use Multiple Reminders

Add calendar alerts, mobile alarms, and SMS reminders for due dates.

Do this for every card you own.

3. Keep Utilization Under 30%

Never use more than 30% of your card’s limit.

This ensures manageable payments and improves your credit health.

4. Keep a Small Emergency Buffer

Maintain a ₹2,000–₹5,000 balance in your account to handle unexpected bills.

5. Review Statements Monthly

Errors happen — sometimes auto-debits fail, or payments don’t reflect.

Always cross-check your statement a week before due date.

Myths & Mistakes About Missing Credit Card Payments

There are tons of half-truths floating around about late payments. Let’s clear them out.

Myth 1: “One day late doesn’t matter.”

Reality: It can. Many banks auto-trigger late fee systems right after the due date.

Myth 2: “If I pay next month, my record resets.”

No. Once reported, it remains in your credit history for years — even if you pay later.

Myth 3: “I’ll just pay minimum due and avoid damage.”

Paying minimum due stops your account from going delinquent but adds massive interest. It’s a trap.

Mistake 1: Ignoring small balances

Even ₹200 unpaid can trigger the same penalties as ₹20,000.

Mistake 2: Relying on recovery agent promises

Never believe verbal assurances. Always get written confirmation for any waivers or settlements.

Mistake 3: Having multiple missed payments across cards

That accelerates your risk profile and reduces your ability to get future credit.

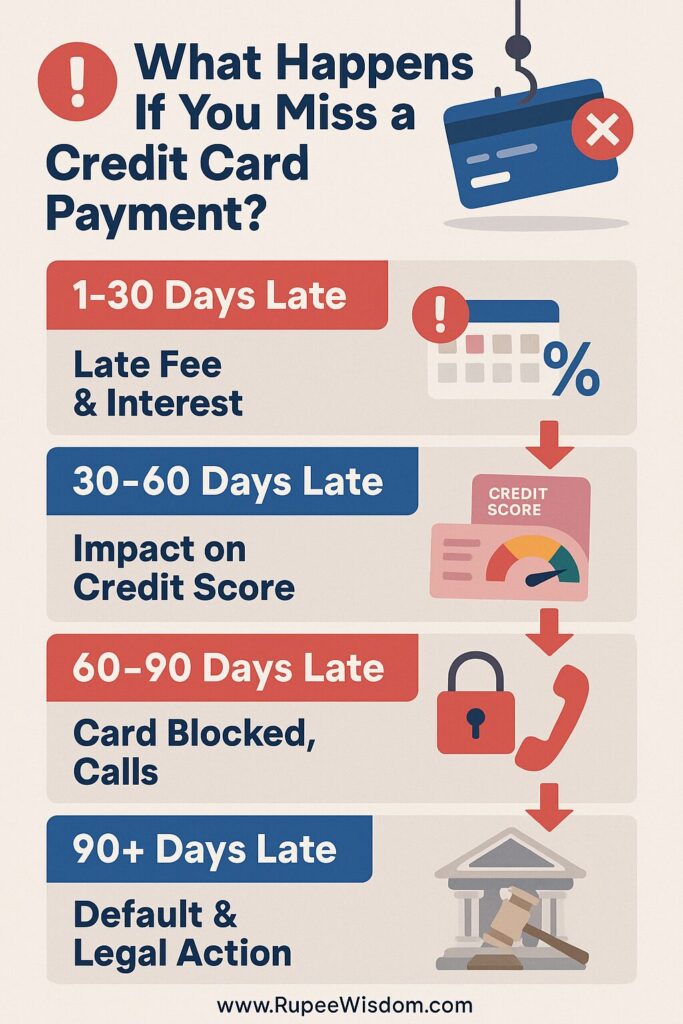

Sample Timeline: How Things Escalate Over Time

| Days Late | What Happens | Damage Level |

|---|---|---|

| 1–3 Days | Grace period, minor interest | Low |

| 4–30 Days | Late fee + interest applies | Moderate |

| 30–60 Days | Reported to credit bureaus, score drops | High |

| 60–90 Days | Card may be blocked, recovery calls start | Severe |

| 90+ Days | Default, legal escalation begins | Critical |

Missing even one due date can start a domino effect — but catching it early can stop the slide.

Conclusion

Missing a credit card payment isn’t rare — but how you handle it decides whether it’s a small stumble or a financial nightmare.

In short:

- Pay something — anything — as soon as you realize you’re late.

- Talk to your bank; they often help if you’re upfront.

- Learn from it — set auto-pay, build discipline, and stay organized.

Ultimately, what happens if you miss a credit card payment depends on how fast you act and how disciplined you stay afterward. Your credit card is a tool, not a trap. Handle it with awareness, and even a missed payment won’t define your financial story.