Searching for laptop on EMI without credit card? You’re not alone. In India, fewer than 6% of people actually own a credit card—but laptops have become essential for work, online classes, freelancing, and even content creation.

The big problem? Laptops aren’t cheap. A decent mid-range machine costs ₹40,000–₹60,000, and high-performance models cross ₹80,000. Not everyone can pay that upfront.

So the obvious question: Can you still buy a laptop on EMI if you don’t own a credit card?

The answer is yes. Today, banks, NBFCs, fintech startups, and even Amazon/Flipkart allow you to split payments into easy EMIs using debit cards, EMI cards, pay-later apps, or consumer loans.

This guide gives you a complete India-specific breakdown:

- All the ways to get laptop EMI without a card

- Costs and risks compared

- Budgeting rules so you don’t overspend

- FAQs that answer every doubt

Let’s dive in.

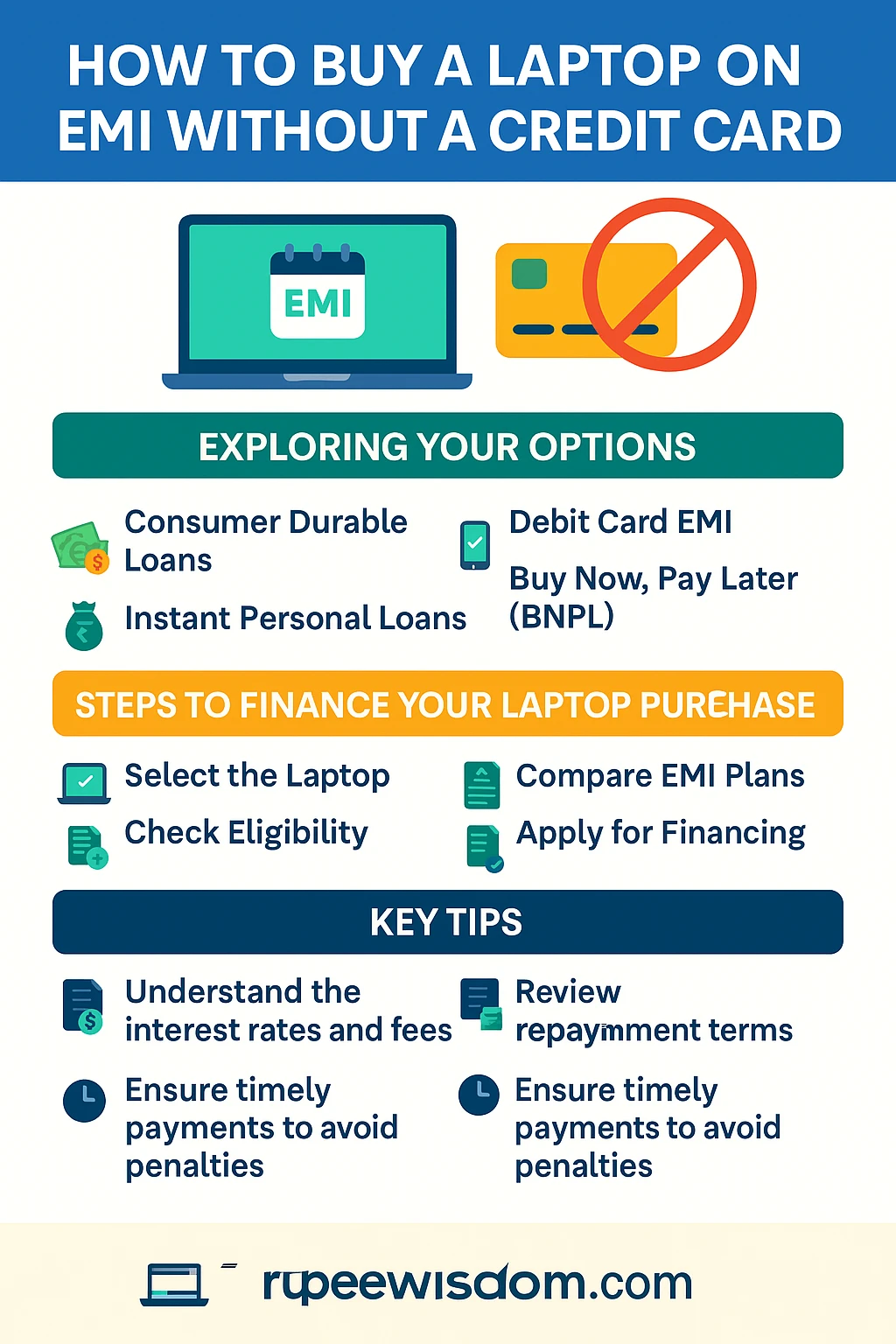

What Does “Laptop on EMI Without Credit Card” Mean?

Traditionally, EMI required a credit card. You swipe the card, choose EMI tenure, and pay installments. But now, India’s fintech and NBFC revolution has unlocked other ways:

- Debit Card EMI → Banks pre-approve certain savings account holders.

- NBFC EMI Cards → Eg. Bajaj Finserv Insta EMI Card.

- Fintech Apps → ZestMoney, Fibe, KreditBee.

- No-Cost EMI on Amazon/Flipkart → Interest is waived by the seller.

- Consumer Durable Loans → Banks/NBFCs give short-term loans for electronics.

Bottom line: your Aadhaar, PAN, salary slip, or bank account activity can qualify you for EMI, even without a credit card.

Top Ways to Buy a Laptop on EMI Without Credit Card in India

1. Debit Card EMI

Debit card EMIs are offered by top banks like SBI, HDFC, ICICI, Axis, and Kotak.

How It Works:

- The bank pre-approves you for a spending limit based on your savings account balance and transaction history.

- You shop online (Amazon/Flipkart) or offline (Croma, Reliance Digital).

- At checkout, select “Debit Card EMI.”

- The bank deducts installments monthly from your account.

Eligibility:

- Must be a pre-approved customer.

- Stable income and active bank account.

- PAN and Aadhaar linked.

Pros:

- No credit card needed.

- Lower interest than fintech apps.

- Quick and convenient.

Cons:

- Not available for everyone.

- Processing fee ₹500–₹1,000.

2. Bajaj Finserv Insta EMI Card

The Bajaj EMI Card is one of the most popular credit-card alternatives in India.

How It Works:

- You apply online or at partner stores.

- Get a pre-approved credit limit (₹10,000–₹4,00,000).

- Buy laptops at partner outlets (Amazon, Flipkart, Croma, Reliance Digital).

- Split payments into 3–24 month EMIs.

Eligibility & Documents:

- Aadhaar, PAN, cancelled cheque.

- Age: 21–60 years.

- Income proof for salaried/freelancers.

Pros:

- Wide acceptance.

- Zero down payment on many laptops.

- Fast approval.

Cons:

- Joining fee (₹500–₹1,000).

- Foreclosure charges if you close early.

3. Fintech Apps & NBFCs

Apps like ZestMoney, Fibe (EarlySalary), KreditBee, TVS Credit are bringing EMI to young India.

How It Works:

- Install app → Complete KYC → Get instant credit line.

- Shop on Amazon/Flipkart and pay via partner EMI.

- Repay in 3–12 months.

Eligibility:

- Aadhaar, PAN, mobile verification.

- Salary slip or bank statement.

- Some approve even without credit history.

Pros:

- Instant approvals.

- Great for freelancers or first-time borrowers.

- No need for an existing bank relationship.

Cons:

- Interest rates 18–30% p.a. (higher than banks).

- Late payment penalties are steep.

4. No-Cost EMI on Amazon & Flipkart

How It Works:

- Seller or brand absorbs the interest.

- You pay just product price ÷ tenure.

- Often available for laptops from HP, Dell, Lenovo, Asus, Apple.

Example:

₹60,000 laptop → 12-month no-cost EMI = ₹5,000/month.

Pros:

- Cheapest option.

- Widely available during sales (Big Billion Day, Great Indian Festival).

Cons:

- Limited to specific brands/offers.

- Sometimes “processing fee” hidden in price.

5. Consumer Durable Loans from Banks

Many banks/NBFCs give short-term loans for gadgets.

How It Works:

- Apply via bank or store finance desk.

- Loan disbursed to retailer directly.

- Repay in 6–24 months.

Pros:

- Structured loan, more formal process.

- EMI auto-debit ensures discipline.

Cons:

- Paperwork heavy.

- Interest 12–18%.

- Approval not instant.

Cost Comparison: ₹40k, ₹50k, ₹60k Laptops

| Laptop Price | Debit Card EMI (12 mo) | Bajaj EMI Card (12 mo) | ZestMoney (12 mo @ 24%) | No-Cost EMI | Durable Loan (12 mo @ 14%) |

|---|---|---|---|---|---|

| ₹40,000 | ~₹3,600 × 12 = ₹43,200 | ₹3,400 × 12 = ₹40,800 | ₹3,900 × 12 = ₹46,800 | ₹3,333 × 12 = ₹40,000 | ₹3,570 × 12 = ₹42,840 |

| ₹50,000 | ~₹4,500 × 12 = ₹54,000 | ₹4,200 × 12 = ₹50,400 | ₹4,800 × 12 = ₹57,600 | ₹4,166 × 12 = ₹50,000 | ₹4,600 × 12 = ₹55,200 |

| ₹60,000 | ~₹5,400 × 12 = ₹64,800 | ₹5,000 × 12 = ₹60,000 | ₹5,800 × 12 = ₹69,600 | ₹5,000 × 12 = ₹60,000 | ₹5,500 × 12 = ₹66,000 |

👉 No-Cost EMI wins if available. Otherwise, Bajaj EMI Card is the next best.

Budgeting Rule for Laptop EMIs

At RupeeWisdom, we always ask: “Can you really afford the EMI?”

Salary vs Safe Laptop EMI (15% Rule)

- ₹20,000 salary → Max EMI ₹3,000

- ₹30,000 salary → Max EMI ₹4,500

- ₹50,000 salary → Max EMI ₹7,500

- ₹75,000 salary → Max EMI ₹11,000

👉 If your EMI exceeds 15% of salary, you risk cash-flow stress.

Pro Tip: Always choose 6–12 months tenure. Longer EMIs keep you stuck in debt.

Risks of Laptop EMI Without Credit Card

- High Interest: Fintech EMIs can cross 24%.

- Hidden Charges: Joining/processing fees, insurance.

- Credit Score Impact: Defaults hurt CIBIL for 7 years.

- Aggressive Recovery: NBFCs may push hard for repayment (though RBI rules apply).

How to Avoid Traps

- Always read the EMI breakdown at checkout.

- Don’t pick longer tenures just for smaller EMIs.

- Keep 1 EMI worth of buffer fund.

- If struggling, request restructuring instead of defaulting.

FAQs on Laptop on EMI Without Credit Card

Q1: Can I buy a laptop on EMI without a credit card?

Yes—using debit card EMI, Bajaj EMI Card, fintech apps, and no-cost EMI.

Q2: Which is the cheapest way?

No-cost EMI on Amazon/Flipkart.

Q3: Can students apply?

Yes—Bajaj EMI Card or fintech apps, but may need co-applicant.

Q4: Will EMI affect my CIBIL?

Yes. On-time = boost; missed = penalty.

Q5: Which banks offer debit card EMI?

SBI, HDFC, ICICI, Axis, Kotak.

Q6: What happens if I default?

Late fees + CIBIL damage + possible recovery calls.

Q7: Is Bajaj EMI Card better than ZestMoney?

Yes—lower cost, wider acceptance, but requires joining fee.

Q8: Can I foreclose early?

Yes, but foreclosure charges apply (varies by lender).

Q9: Do all laptops qualify for EMI?

Most mid/high-range laptops do, but check seller terms.

Q10: Are EMI apps safe?

Stick to RBI-registered NBFC partners for safety.

Final Word

Buying a laptop on EMI without credit card is no longer difficult. From debit card EMIs to Bajaj EMI Cards, fintech apps, and no-cost offers, India has options for everyone.

But remember: EMI = loan. Use the 15% salary rule, prefer no-cost EMI, and never ignore terms. Done smartly, you can walk away with your dream laptop without sinking into debt.

👉 Ready to buy? Check Amazon and Flipkart for the latest laptops on EMI without credit card or apply for a Bajaj EMI Card to unlock zero down payment deals.