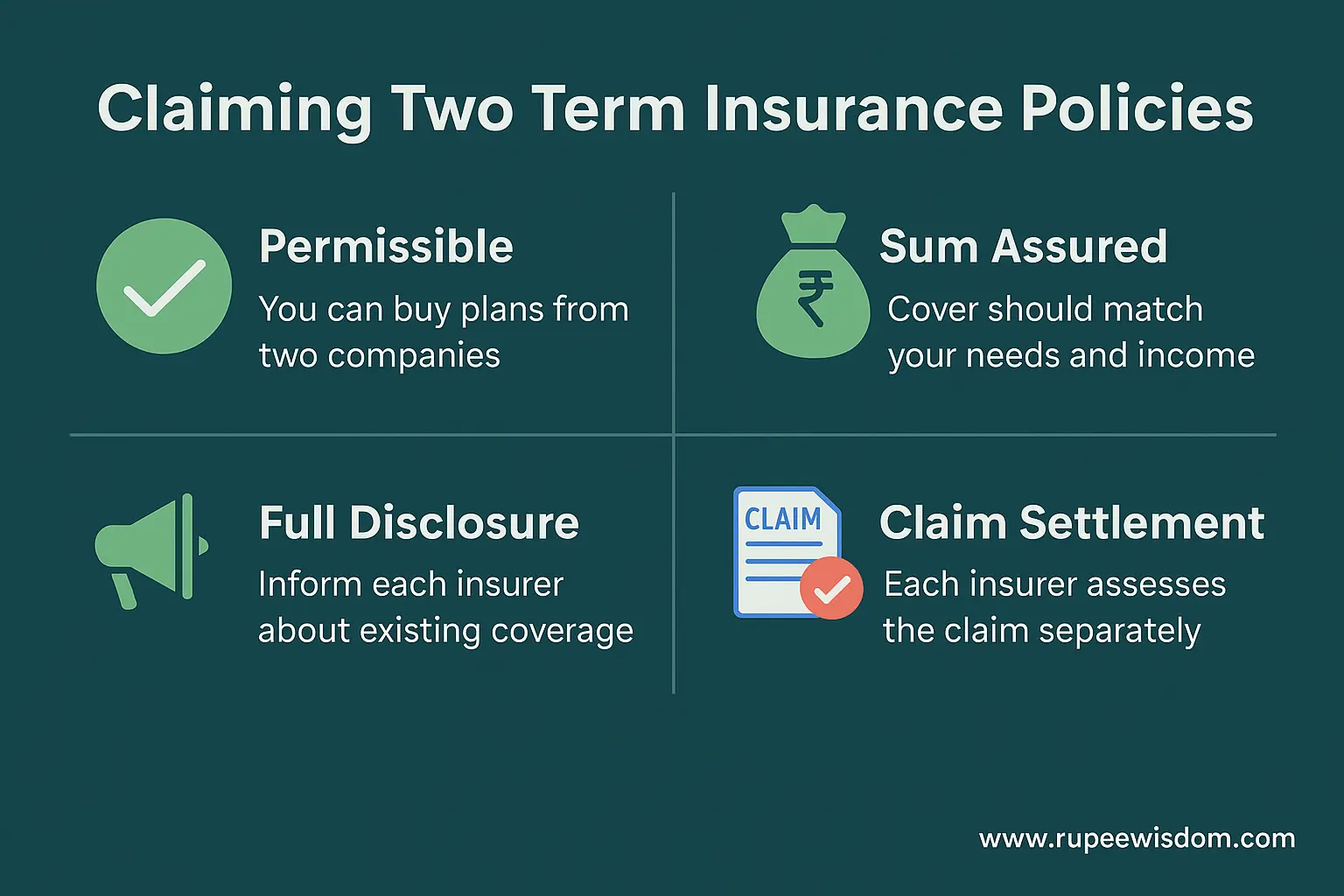

Yes, you can claim from 2 term insurance policies in India. If the insured had more than one valid term plan, the nominee can file a separate claim with each insurer and receive the respective payouts. This is possible provided all disclosures were made honestly during purchase and the claim meets each policy’s terms.

Can We Claim 2 Term Insurance from Two Companies in India?

Holding more than one term policy is permissible in India, and nominees can claim from each insurer independently. Each policy is a separate contract, and insurers process claims individually. The only common pitfall is non-disclosure. If earlier policies or medical history were not declared when buying a new policy, there can be disputes during claim settlement.

Is It Legal to Have Multiple Term Insurance Policies?

Yes, there is no restriction under Indian law on holding multiple term policies. The total cover is underwritten based on the individual’s income, liabilities, and overall insurability. As long as the sum assured is justifiable, multiple policies are acceptable.

How Claims Work with 2 Term Policies

- Claim Intimation: Notify each insurer separately through their claim portal, branch, or email.

- Submit Documents: Provide claim form, death certificate, ID proofs, policy documents, and hospital/police records if required.

- Independent Assessment: Each insurer reviews the claim individually as per its terms.

- Separate Payouts: Each valid policy pays its full sum assured to the nominee.

There is no sharing or splitting of payouts between companies. Each policy pays the promised sum if the claim is genuine.

Benefits of Holding Two Term Insurance Policies

- Flexibility: Cover can be layered, for example, one long-term family policy and one shorter-term policy linked to a home loan.

- Insurer Diversification: If one claim takes longer, the other may get processed earlier.

- Feature Mix: Different policies may offer unique features or riders, such as life-stage benefit, critical illness, or accidental death riders.

Limitations to Keep in Mind

- Administrative Effort: Multiple policies mean more renewals, documents, and nominee management.

- Disclosure Requirement: All existing policies and health details must be disclosed at the time of purchasing a new policy.

- Underwriting Checks: Higher aggregate coverage must align with income and liabilities.

Importance of Full Disclosure

Honesty in declarations is the most critical factor. At the time of buying an additional policy, the following must always be disclosed:

- Existing policy numbers, insurers, and sum assureds

- Accurate income, occupation, and liabilities

- Past and current medical conditions, including lifestyle habits

Non-disclosure is one of the most common reasons for claim rejection.

Claiming from Two Companies: Step-by-Step

- Collect documents: death certificate, ID proofs, hospital or police records, and policy copies.

- File claim intimation with each insurer.

- Submit required documents to each insurer separately.

- Track claim acknowledgments and payout details.

- Escalate unresolved issues through the insurer’s grievance redressal or the IRDAI grievance portal.

Common Questions

Can both insurers pay full claims?

Yes. Each insurer pays its full sum assured independently if the claim is valid.

Will payouts be split?

No. Term insurance is a benefit-based product. Each policy pays its own contracted sum assured.

What if I did not disclose an earlier policy?

Non-disclosure can result in investigation and possible repudiation. Always disclose existing cover.

Is there a limit to the number of term policies I can buy?

There is no limit, but the total cover must match your financial profile.

Can fraud across policies be caught?

Yes. Claim verification is rigorous, and fraudulent claims may attract legal action.

Real-Life Scenarios

Case 1: Clean Disclosure

A person holds two policies, one for ₹1 crore and another for ₹50 lakh. Both were disclosed at purchase, and all health information was provided. On death, the nominee claims from both insurers and receives the full ₹1.5 crore.

Case 2: Non-Disclosure

A policyholder purchased a second policy but did not declare the first one. On claim, the insurer discovers the omission, delaying or denying settlement.

Case 3: Health History Hidden

A buyer concealed a pre-existing illness. Regardless of multiple policies, material non-disclosure can lead to rejection.

Documentation Checklist

- Insurer-specific claim form

- Death certificate (original or attested copy)

- Nominee’s ID and address proof

- Policy document copy

- Medical and hospital records

- Police documents (if accidental or suspicious death)

- Bank details for payout

When Two Term Policies Make Sense

- One long-term policy for overall family protection, plus a shorter policy to cover specific liabilities like a loan.

- A mix of features, such as life-stage increase in one plan and riders in another.

- Diversification across insurers to reduce dependency on a single company.

Tips for Smooth Claims if You Have Multiple Policies

- Keep a single “claim kit” folder with all essential documents.

- Ensure nominations are correct and updated on each policy.

- Maintain a policy summary sheet with policy numbers, sums assured, claim URLs, and nominee details.

- Review cover annually to match changing income and liabilities.

Myths and Facts

- Myth: If you have 2 policies, insurers will share and pay less.

Fact: Each policy pays its full sum assured. - Myth: Existing policies need not be disclosed.

Fact: Non-disclosure is a major cause of claim denial. - Myth: There is a legal cap on the number of policies.

Fact: No such cap exists; underwriting is based on income and liability justification. - Myth: Fraudulent claims won’t be caught if split across insurers.

Fact: Claim investigations are strict, and fraud attracts penalties.

Final Word

Yes, it is possible to claim 2 term insurance policies from two companies in India. Each insurer is bound by its own contract, and nominees can receive the full payout from both if the claim is valid and disclosures were made honestly. The keys to smooth claim settlement are full disclosure, proper documentation, and timely claim filing.

Holding two policies can be useful for layered cover and diversification, but it requires careful management. Always declare existing policies, keep your documents ready, and review nominations regularly.