When life changes, your term insurance cover should too. That’s the promise of the life stage benefit in term insurance — a feature that allows you to increase your life cover as your responsibilities grow, without juggling multiple policies or undergoing fresh medical tests each time.

In this in-depth guide, we’ll explain what life stage benefit is, how it works in India, its pros and cons, and how to choose the right plan. By the end, you’ll know if this feature is a must-have for your family’s financial safety.

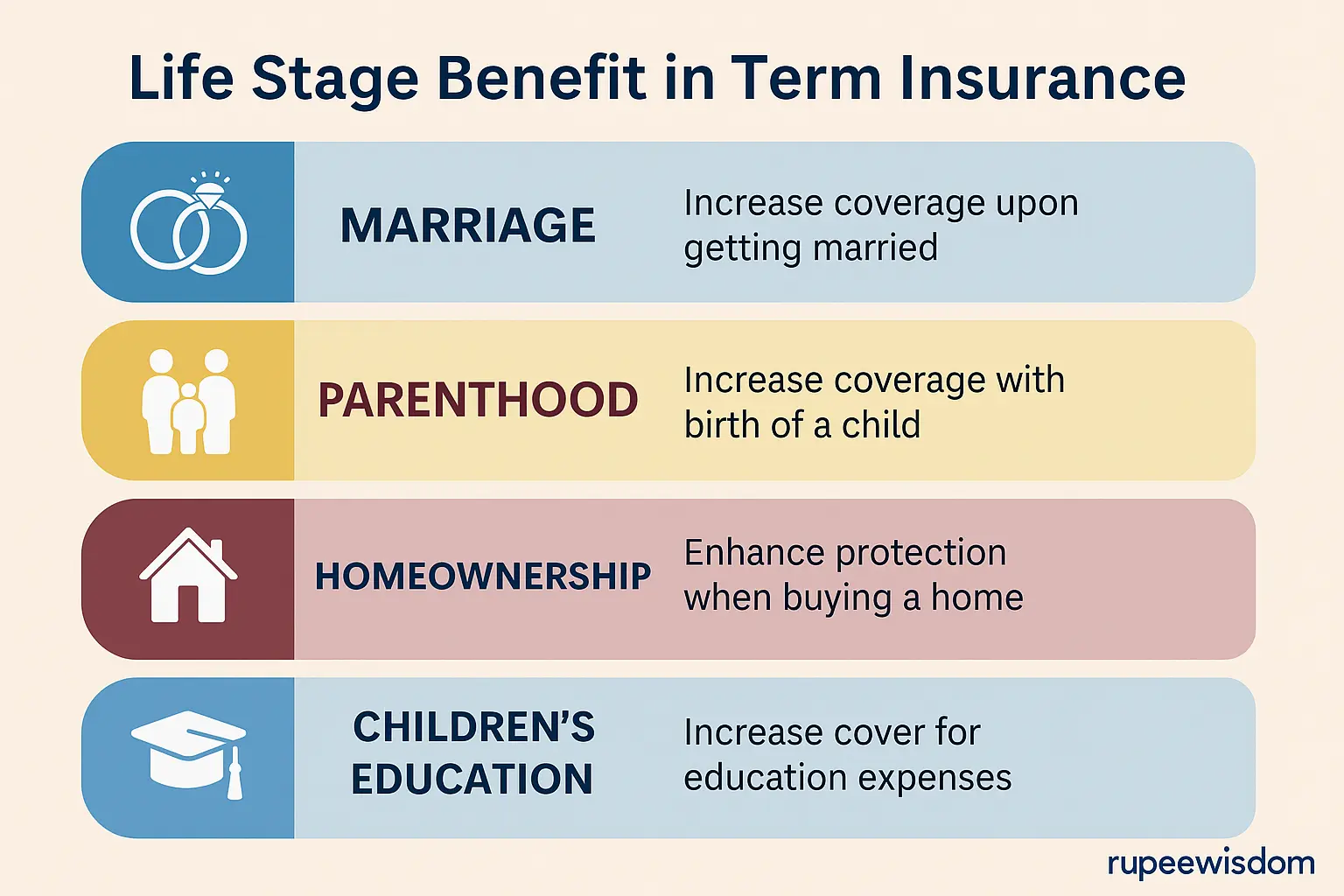

What Is Life Stage Benefit in Term Insurance?

In simple terms, life stage benefit in term insurance lets you increase your policy cover at specific milestones like:

- Marriage

- Birth/adoption of a child

- Taking a large loan (like a home loan)

The idea is straightforward: when your responsibilities grow, your cover should grow too. Instead of buying a new term plan, you can top-up your existing one under predefined rules.

How Does the Life Stage Benefit Work?

Here’s the typical flow in India:

- Buy a base term plan that includes the life stage option.

- Triggering event occurs (marriage, child birth, major loan).

- Request increase within the allowed time window (usually a few months from the event).

- Medical tests may not be required for the incremental cover if you meet the insurer’s conditions.

- Premium increases only for the added cover for the remaining policy term.

Example:

- Base policy: ₹1 crore cover at age 26.

- At marriage (age 30): add ₹50 lakh.

- At first child (age 33): add ₹25 lakh.

- At second child (age 36): add ₹25 lakh.

Total cover = ₹2 crore under one policy, without new underwriting each time.

Benefits of Life Stage Benefit in Term Insurance

- Flexibility: Your cover grows as your life evolves.

- No Medical Hassle: Many insurers waive medicals for increments if requested in time.

- Cost-Effective: You pay premium only on the extra cover, not a whole new base.

- Convenience: One policy, one schedule, fewer documents.

- Future-Proofing: Protects your family when your income, dependents, and liabilities increase.

Limitations You Should Know

- Event-based: Increases allowed only for specified events.

- Caps Apply: Typically, +50% at marriage, +25% for first child, +25% for second child, subject to max limits.

- Premium Rise: Extra cover means higher premium, though only on the increment.

- No Cover Reduction: You can’t scale down later.

- Not in All Plans: Some term plans in India don’t offer this feature.

Life Stage Benefit vs Buying a New Term Policy

| Factor | Life Stage Benefit | Buying a New Policy |

|---|---|---|

| Medical Tests | Often not required for increments | Fresh underwriting needed |

| Administration | One policy, easy tracking | Multiple policies, more hassle |

| Premiums | Only on the incremental cover | Higher, since new base starts at current age |

| Speed | Faster if event docs ready | Slower due to full application |

| Flexibility | Limited to certain events | Can buy anytime |

Who Should Opt for Life Stage Benefit in Term Insurance?

- Young professionals just starting out.

- Newly married couples.

- Parents planning children.

- Families taking big home or business loans.

If you expect your financial responsibilities to grow, this feature can be a game-changer.

Which Term Plans in India Offer Life Stage Benefits?

Several leading insurers include this feature in select plans. For example:

- ICICI Pru iProtect Smart – allows cover increases at marriage, first child, and second child.

- SBI Life – positions life stage as “coverage that adapts to your milestones.”

- Bajaj Allianz Life – markets life stage as a flexible cover increase option.

- Tata AIA – highlights that life cover should grow as needs grow.

Always read the latest brochure — percentages, limits, and terms differ across insurers.

Things to Check Before Opting

- Event Windows: How long do you have to request the increase?

- Maximum Caps: Both percentage and rupee amount limits.

- Medical Rules: Clear mention of “no medicals” for increments.

- Premium Calculation: How the extra premium is loaded.

- Plan Variants: Some plan versions may exclude life stage.

Always review the policy brochure carefully and cross-check the latest rules on the IRDAI official website before finalizing your plan.

Common Mistakes to Avoid

- Missing the time window: Results in medicals or denial.

- Assuming unlimited increases: Caps always apply.

- Skipping documentation: Proof of marriage, child, or loan required.

- Over-insuring: Aim for 10–15× your annual income plus liabilities.

FAQs on Life Stage Benefit in Term Insurance

Does the life stage benefit always avoid medicals?

Not always — only if conditions and timelines are met.

Q. What documents do I need?

Marriage certificate, child birth/adoption certificate, or loan sanction letter.

Q. Is it cheaper than buying a new plan?

Usually yes, as you’re only paying for the increment.

Q. Which insurers in India offer it?

Several, including ICICI, SBI, Bajaj Allianz, Tata AIA.

Q. What if I miss the deadline?

You may need full underwriting or a new policy.

Final Word: Why Life Stage Benefit Matters

The life stage benefit in term insurance is one of the smartest ways to keep your family protected as life changes. It adapts your cover to marriage, children, and big loans, while sparing you the hassle of new policies and fresh medicals.

If you’re in your 20s or 30s, this feature is worth prioritizing when you choose a plan. One decision now can save you cost, effort, and sleepless nights later.